This Australian Charities Report is the annual analysis of the information we receive from charities in their Annual Information Statements. This is the 9th edition.

Foreword

I am delighted to present the ninth edition of the Australian Charities Report – my first as Commissioner.

This is a project close to my heart as I believe data makes an important contribution to strategy, policy development and decision-making.

The Australian Charities Report – our annual analysis of the charity sector – maps the size and scope of the sector, illustrating the contribution of Australia’s charities to the economy and to communities locally and overseas.

In our tenth year, it was timely for us to review the purpose, format and content of the report, in consultation with key stakeholders, to ensure it continues to be the best resource possible for the sector.

We must adapt our approach to conduct the most relevant analysis and will continue to finesse our approach in consultation with our stakeholders. We have made some changes, including more state-based analysis, comparisons with data from the 2018 Australian Charities Report and increased data visualisation.

As philanthropy is part of the current national conversation, with a Productivity Commission review taking place, I am pleased to present our ‘Focus on giving and philanthropy’ in this report.

Our data confirms not only that philanthropists are significant in number – nearly one fifth of registered charities are grant makers – but they also play a very significant role in funding those charities we regulate.

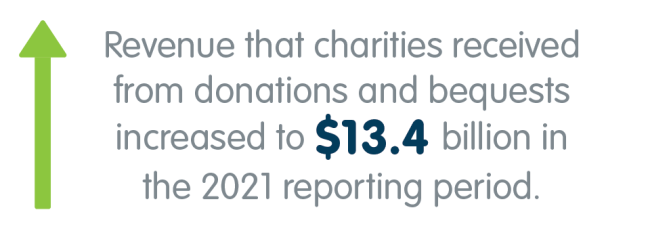

The data also shows that $13.4 billion of charity revenue is made up of donations and bequests, and charities distributed $9.7 billion in grants and donations.

The report is based on the most current data available for Australia’s registered charities and builds on analysis from previous years. For this edition, we looked at the Annual Information Statements of 49,402 charities from the 2021 reporting period.

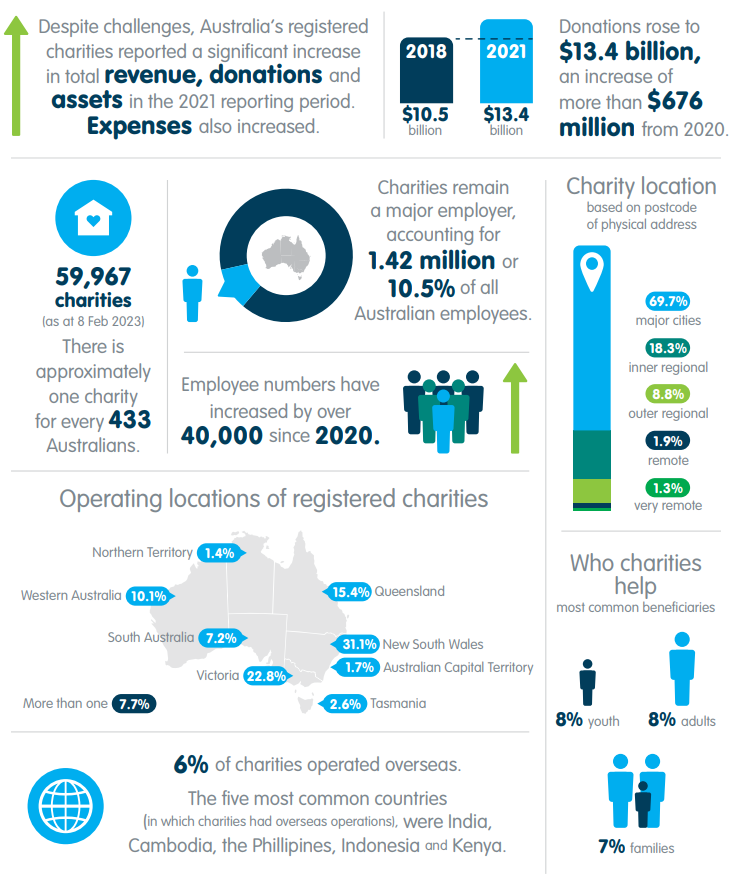

While challenges for the sector continued in 2021, such as increased costs of delivery resulting from inflation, revenue, assets and donations grew. Total revenue from those charities reporting to the ACNC rose to $190 billion, an increase of $14 billion on the previous year. Charity assets increased by $31 billion to a total of $422 billion, and donations increased by $676 million to a total of $13.4 billion.

Expenses increased by $7.1 billion to a total of $175 billion. Overall, employee expenses continued to be a significant expense for charities. The sector remains a major employer – with charity employees accounting for 10.5% of the Australian workforce. Charities gained over 40,000 employees in the 2021 reporting period, taking the total number added since 2018 to over 111,000.

Volunteers continue to underpin the work of the sector and 50% of charities operate with no paid staff.

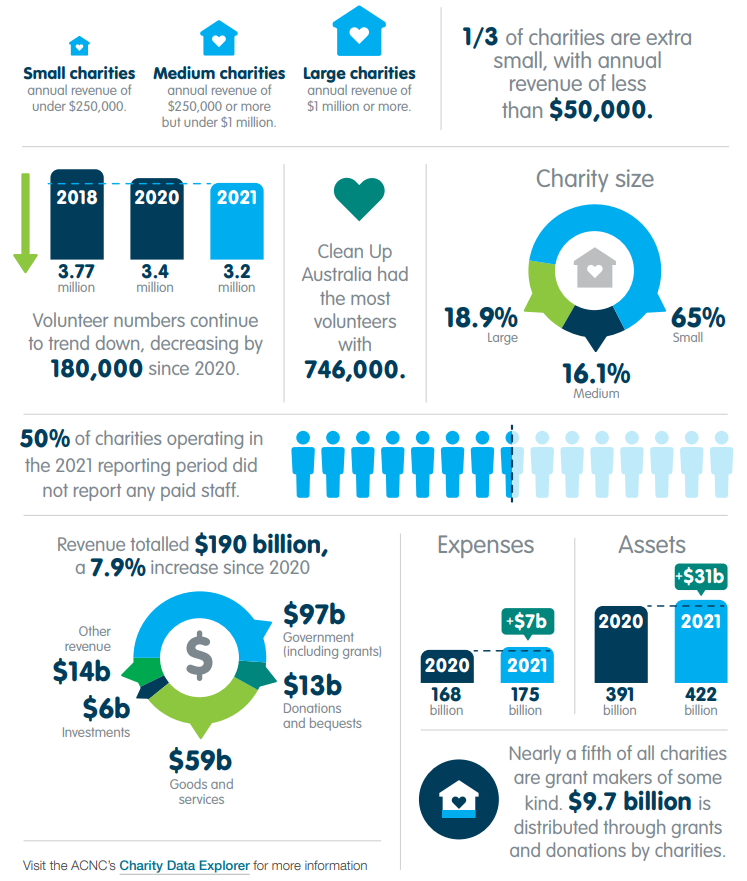

However, the report confirms the widely observed decline in Australian volunteering, with volunteer numbers dropping to 3.2 million from 3.4 million in 2020. The picture is more sobering when we look at the data from 2018, which shows a loss of more than half a million volunteers (596,000) between then and now.

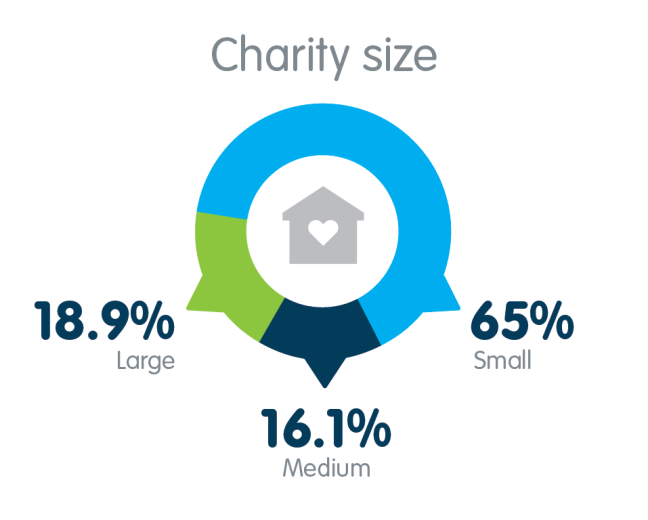

Behind the topline figures are thousands of small charities operating with mostly volunteer staff. In fact, most charities are small (65%) with revenue of under $250,000, and a third of all charities operate on less than $50,000 annual revenue with very few paid employees – 53.9% of small charities and 88.3% of extra small charities operate with no paid staff.

I invite you to read the report for a comprehensive picture of the status of Australia’s charities and the valuable contribution they make to all facets of life. I also want to highlight that our Charity Data Explorer allows you to undertake customised searches relevant to specific subsectors areas of interest.

Warm regards,

Sue Woodward AM

Commissioner

Australian Charities and Not-for-profits Commissioner

This edition of the annual Charities Report is based on information submitted in the 2021 Annual Information Statements (AIS) of 49,402 charities.

The Australian Charities and Not-for-profits Commission Act 2012 (Cth) (the ACNC Act) requires registered charities to submit an Annual Information Statement for each financial year.

The Annual Information Statement collects a range of data about charities, including their programs and activities, finances and staff.

This year the Australian Charities Report includes some new observations including:

- time series data from the Australian Charities Report 2018 which analysed data from the 2018 Annual Information Statement

- a focus on giving and philanthropy, which looks at Australia’s grant making charities.

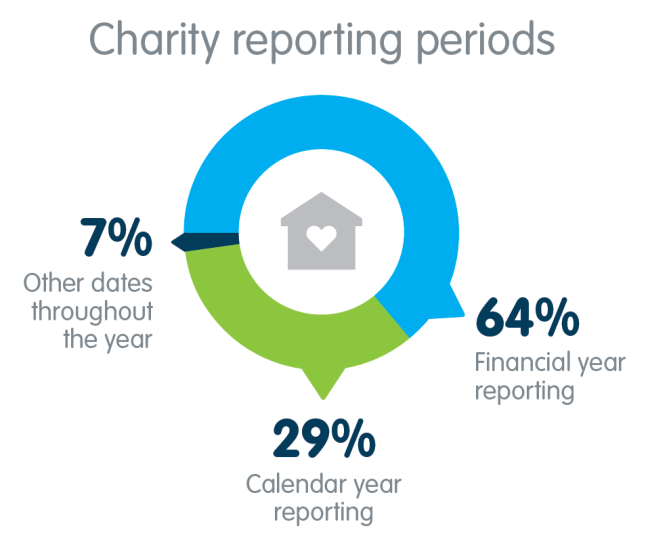

The 2021 Annual Information Statement reporting period for most charities was either the financial year of 1 July 2020 – 30 June 2021 or the calendar year of 1 January 2021 – 31 December 2021.

Of the submissions analysed for this report:

- 31,582 charities (64%) had a financial year reporting period

- 14,170 charities (29%) had a calendar year reporting period

- 3,650 charities (7%) had reporting periods that ended on other dates throughout the year.

Charity reporting periods

Charities have up to six months after the end of their reporting year to submit their Annual Information Statement and financial report (if required).

For non-government schools, we have an optional arrangement with the Department of Education (DoE) that streamlines their reporting process. The DoE provides us with financial information each year that we use to complete the Annual Information Statements of non-government schools that use this arrangement.

Some Aboriginal and Torres Strait Islander organisations are registered as corporations under the Corporations (Aboriginal and Torres Strait Islander) Act 2006 (Cth) (CATSI Act). These corporations are regulated by the Office of the Registrar of Indigenous Corporations (ORIC) and are not required to report to the ACNC so are excluded from this report.

There are approximately 60,000 registered charities in Australia.

According to the Australian Bureau of Statistics, Australia’s population was 25,978,935 people at 30 June 2022. This equates to approximately one charity for every 433 Australians.

Australia’s charity sector comprises charities of different sizes – from tiny local community groups to large universities and international aid organisations.

For the 2021 Annual Information Statement, the ACNC classified charities into three size categories:

A charity’s size is based on its total annual revenue for a reporting period.

Analysing charity size helps us understand the scale of charities’ operations and provides an insight into the composition of the sector over time.

The distribution of sizes across the charity sector has remained stable since the first edition of the Australian Charities Report in 2013.

For the 2022 and later Annual Information Statements, the annual revenue thresholds for size classification have changed to less than $500,000 for small charities, $500,000 or more, but under $3 million for medium charities and $3 million or more for large charities.

Additional breakdown of charity size

To provide greater insight into Australia’s charity sector, this report presents three additional charity size categories:

- Extra small charities – annual revenue less than $50,000

- Very large charities – annual revenue of $10 million or more but less than $100 million

- Extra large charities – annual revenue of $100 million or more.

In the 2021 reporting period, the percentage of extra small charities increased by 0.2% over the previous year.

Table 1: Australian charities by charity size (additional categories) with changes from the previous reporting period.

| Charity size | Total revenue | % of charities | % of change from previous year | % of change over 3 years |

|---|---|---|---|---|

| Extra small | Less than $50,000 | 31.6 | +0.2 | +1.2 |

| Small | $50,000 or more but less than $250,000 | 20.3 | -0.5 | -0.7 |

| Medium | $250,000 or more but less than $1 million | 14.1 | +0.4 | +0.2 |

| Large | $1 million or more but less than $10 million | 13.4 | -0.3 | 0.0 |

| Very large | $10 million or more but less than $100 million | 4.5 | +0.1 | +0.1 |

| Extra large | $100 million or more | 0.5 | +0.1 | +0.1 |

| Size unknown (BRC) | 15.7 | 0.0 | -1.2 |

A Basic Religious Charity (BRC) is a type of religious charity that meets specific requirements. Basic Religious Charities are not required to answer the financial questions in the Annual Information Statement, nor submit annual financial reports or comply with Governance Standards.

In their 2021 Annual Information Statement, 8,280 charities (17% of all charities) reported being a Basic Religious Charity. This is 320 fewer than in 2018, when 8,600 identified as Basic Religious Charities.

If a Basic Religious Charity voluntarily provided financial information in its 2021 Annual Information Statement, it was included in the financial analysis of this report.

In the 2021 Annual Information Statement, 7,743 Basic Religious Charities did not provide financial information. In this report, the size of these Basic Religious Charities is noted as ‘Size Unknown (BRC)’ where relevant.

Table 2: All Basic Religious Charities by ACNC charity size

| Charity size | % of Basic Religious Charities | % change over 1 year | % change over 3 years |

|---|---|---|---|

| Small | 82.7 | +0.1 | -0.8 |

| Medium | 13.7 | -0.1 | +0.7 |

| Large | 3.6 | 0.0 | +0.1 |

To explore charity size further visit our Charity Data Explorer.

Charities that were not operating

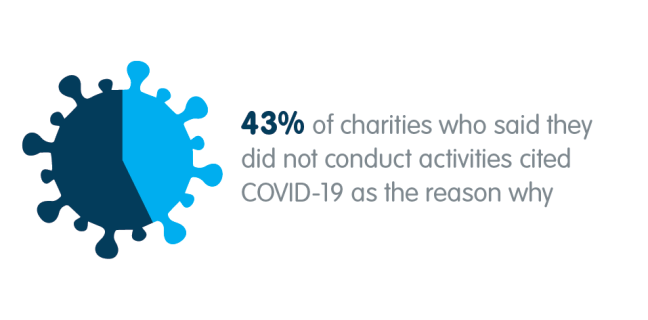

The number of charities not operating rose in the 2021 Annual Information Statement. Four percent of charities (just over 2,000 in total) reported that they did not conduct activities during the period.

In the 2021 Annual Information Statement, more than 860 of these charities – 43% of all charities who said they did not conduct activities – cited COVID-19 as the reason why.

Other charities that reported no activities were either winding up, conducting activities in the name of another charity, had no funding, reported they had insufficient staff or volunteers available, or were still in a planning or establishment phase and had yet to begin activities.

We base a charity’s location on the physical address provided by the charity. This is most commonly the physical base for the charity – for example, a head office – and may be distinct from the places in which it conducts its activities.

This analysis includes all registered charities that have provided a physical address to us. Some caution should be taken when comparing results from previous editions of the Australian Charities Report, as earlier editions only included those charities that submitted an Annual Information Statement.

Table 3: Charity location (based on postcode of physical address)

| Location in Australia | % of charities |

|---|---|

| Major cities | 69.7 |

| Inner regional | 18.3 |

| Outer regional | 8.8 |

| Remote | 1.9 |

| Very remote | 1.3 |

Locations are derived using the measure in the Australian Statistical Geography Standard (ASGS): Volume 5 – Remoteness Structure.

Operations in Australia

In all states and territories, except Queensland, the proportion of charities is similar to that state or territory’s proportion of Australia’s overall population.

Queensland’s proportion of charities is less than its proportion of Australia’s population.

Table 4: Operating locations of registered charities

| State or territory | % of charities | % of Australia's population at 30 June 2022 |

|---|---|---|

| ACT | 1.7 | 1.8 |

| NSW | 31.1 | 31.4 |

| NT | 1.4 | 1.0 |

| QLD | 15.4 | 20.5 |

| SA | 7.2 | 7.0 |

| TAS | 2.6 | 2.2 |

| VIC | 22.8 | 25.5 |

| WA | 10.1 | 10.7 |

| More than one | 7.7 | - |

Operations overseas

Our analysis shows that approximately 6% of charities reported that they operated overseas in the 2021 Annual Information Statement.

Of these charities, 69% reported operating in just one country or region and 31% in more than one. For charities that operated in more than one, 13% reported operating in five or more countries or regions and 5% in ten or more.

Charities reported operating in 199 different countries or regions (excluding Australia). The five most common countries were India, Cambodia, the Philippines, Indonesia and Kenya.

State and territory breakdown

The state and territory breakdown uses a charity’s physical address (where we have been provided with it) and data from the 2021 Annual Information Statement.

Around 8% of charities operate in multiple jurisdictions, but this may not be reflected by a charity’s physical address.

This is relevant for the analysis of volunteers; although volunteers are attributed to a state based on a charity’s street address, the figures include volunteers across Australia.

Table 5: Charity revenue source, volunteers and employees by state or territory

| State or territory | Number of charities | Revenue from government ($ million) |

Revenue from donations and bequests ($ million) | Revenue from goods or services ($ million) | Total revenue ($ million) | Volunteers | Employees |

|---|---|---|---|---|---|---|---|

| ACT | 1,106 | 1,697 | 154 | 1,043 | 3,531 | 48,711 | 26,943 |

| NSW | 15,727 | 24,499 | 5,149 | 13,560 | 49,996 | 1,487,020 | 337,237 |

| NT | 436 | 1,284 | 27 | 571 | 2,026 | 11,053 | 12,547 |

| QLD | 6,898 | 11,424 | 1,639 | 7,782 | 22,510 | 369,673 | 174,778 |

| SA | 3,370 | 5,436 | 391 | 3,395 | 10,238 | 140,989 | 94,936 |

| TAS | 1,053 | 2,074 | 107 | 783 | 3,215 | 48,815 | 29,882 |

| VIC | 11,491 | 24,664 | 2,979 | 12,738 | 44,633 | 521,317 | 300,280 |

| WA | 4,247 | 8,551 | 657 | 7,190 | 17,656 | 200,967 | 143,528 |

Note: Charities that report as part of a group have been excluded from this analysis.

To find out more about where charities are located visit our Charity Data Explorer.

To be registered with the ACNC, a charity must have a charitable purpose. This purpose is the reason a charity operates.

A charity may conduct a range of activities and services (programs) to achieve its purpose or purposes.

Our activity classification system is based on CLASSIE (Classification system of Australian Social Sector Initiatives and Entities), which was specifically developed by Our Community for the social sector. By removing some non-charitable classifications, we refined the CLASSIE system to include a taxonomy suitable for the work of charities.

In 2021 all charities were required to provide details of a minimum of one program in their Annual Information Statement and had the option to provide details of up to 10 programs.

Our analysis is limited to the approximately 82,000 programs that charities detailed. This figure may not represent the full number of programs that charities conduct, as some may have only provided details on one of their programs.

Number of programs reported

Charities can select from 857 classifications for their programs – this is the way we obtain information about their activities.

Charities reported an average of 1.7 programs in the 2021 reporting period. The average number of programs reported increased as charity size increased: extra small charities and Basic Religious Charities reported an average of 1.4 programs, while extra large charities reported an average of 3.4 programs.

The most common program classifications were religion and faith-based spirituality, human services, and education. This corresponds with the second and third most common charities by subtype category being advancing education and advancing religion (see the ‘Charity subtypes’ section).

Table 6: Number and percentage of programs by charity size

| Charity size | Number of programs | % of total programs |

|---|---|---|

| Extra small | 20,184 | 24.5 |

| Small | 16,804 | 20.4 |

| Medium | 13,738 | 16.7 |

| Large | 14,892 | 18.1 |

| Very large | 5,795 | 7.0 |

| Extra large | 822 | 1.0 |

| Size unknown (BRC) | 10,110 | 12.3 |

| Grand total/average | 82,345 | 100.0 |

Activity categories

CLASSIE is a nested taxonomy to classify social sector initiatives using four levels of granularity, with one being the highest level (e.g. arts and culture) and four being the most granular (e.g. musical theatre).

The following analysis is based on CLASSIE’s level one activity classifications that registered charities select from to create searchable metadata about what they do for users of the Charity Register program search. All 857 classifications can be attributed to a level one classification.

In the 2021 Annual Information Statement, the most common classification across all charity sizes was religion and faith-based spirituality (approximately 17,700 programs), followed by human services (approximately 13,100 programs) and education (approximately 12,800 programs).

The least common categories were social sciences, science, and international relations. The distribution of charities across classification types is consistent with the previous year’s reporting, with one exception, community development increased by 1.5%, likely due to the ACNC’s addition of the new ‘grant making’ classification.

Programs classified as religion and faith-based spirituality were more prevalent among smaller charities, while programs classified as human services or education were more common among larger charities.

Table 7: CLASSIE level one classifications reported by charities

| CLASSIE classification | Number of programs | % |

|---|---|---|

| Agriculture, fisheries and forestry | 669 | 0.8 |

| Animal welfare | 1,403 | 1.7 |

| Arts and culture | 5,938 | 7.2 |

| Community development | 7,974 | 9.7 |

| Economic development | 1,952 | 2.4 |

| Education | 12,855 | 15.6 |

| Environment | 2,272 | 2.8 |

| Health | 9,256 | 11.2 |

| Human rights | 1,268 | 1.5 |

| Human services | 13,080 | 15.9 |

| Information and communications | 650 | 0.8 |

| International relations | 355 | 0.4 |

| Public affairs | 973 | 1.2 |

| Public safety | 1,975 | 2.4 |

| Religion and faith-based spirituality | 17,673 | 21.5 |

| Science | 245 | 0.3 |

| Social sciences | 123 | 0.1 |

| Sport and recreation | 1,341 | 1.6 |

| Unknown or not classified | 2,343 | 2.8 |

| Total | 82,345 | 100.0 |

Table 8: Most common classification by charity size

| Charity size | Most common classification | Second most common classification | Third most common classification |

|---|---|---|---|

| Extra small | Education (16%) | Community development (15%) | Religion and faith-based spirituality (13%) |

| Small | Religion and faith-based spirituality (21%) | Education (15%) | Human services (14%) |

| Medium | Education (18%) | Human services (17%) | Religion and faith-based spirituality (13%) |

| Large | Human services (23%) | Education (19%) | Health (15%) |

| Very large | Human services (31%) | Education (23%) | Health (21%) |

| Extra large | Human services (40%) | Education (20%) | Health (19%) |

Charities were able to select multiple beneficiaries for each program they reported.

Our analysis is limited to the approximately 82,000 programs that charities reported. This figure may not represent the full number of programs that charities conducted, as charities only had to report on one program, although they could include details of up to 10 programs.

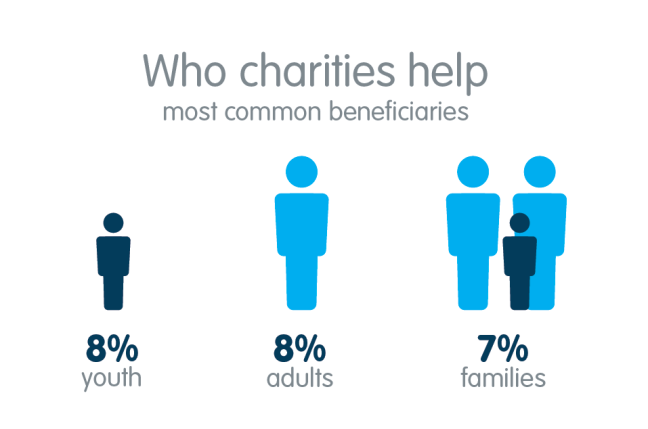

Overall, the most common beneficiaries were:

- Adults – aged 25 to under 65 (8%)

- Youth – aged 15 to under 25 (8%)

- Families (7%)

Table 9: Most common beneficiaries by charity size

| Charity size | Most common beneficiary | Second most common beneficiary | Third most common beneficiary |

|---|---|---|---|

| Extra small | Adults – aged 25 to under 65 (9%) | Youth – aged 15 to under 25 (8%) | Families (8%) |

| Small | Adults – aged 25 to under 65 (8%) | Youth – aged 15 to under 25 (8%) | Families (8%) |

| Medium | Adults – aged 25 to under 65 (8%) | Youth – aged 15 to under 25 (8%) | Families (7%) |

| Large | Youth – aged 15 to under 25 (8%) | Adults – aged 25 to under 65 (7%) | Females (6%) |

| Very large | Youth – aged 15 to under 25 (9%) | Adults – aged 25 to under 65 (7%) | Children – aged 6 to under 15 (7%) |

| Extra large | Youth – 15 to under 25 (10%) | Adults – aged 25 to under 65 (9%) | Adults – aged 65 and over (9%) |

Note: Basic Religious Charities were excluded from the table because their sizes are unknown. To meet the requirements of a Basic Religious Charity, a charity must have the sole purpose of ‘advancing religion’.

To find out more about what charities do and who they help, visit our Charity Data Explorer or search the Charity Register.

Volunteers

Volunteering remains a vital part of the charity sector, with charities reporting that 3.2 million volunteers helped deliver services in the 2021 reporting period.

While the total number remains high, it is a decrease of approximately 180,000 on the previous reporting period and of approximately 596,000 from 2018 when charities reported 3.77 million volunteers.

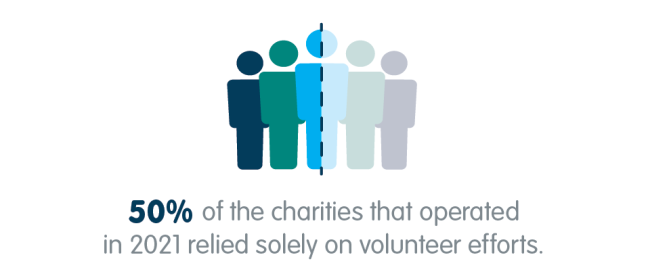

Despite a reduction in the number of volunteers reported, 50% of the charities that operated in 2021 reported having no paid staff – meaning they relied solely on volunteer efforts.

It is important to note that the figure of 3.2 million does not reflect the total number of individual volunteers across Australia. This is because people may volunteer for more than one charity, and many more volunteer for not-profits that are not charities, such as their local sporting clubs.

Employees

The Annual Information Statement asks each charity to provide a snapshot of its employment figures based on its most recent pay period.

The charity sector remained a significant employer in Australia with charities reporting 1.42 million paid employees in the 2021 reporting period.

In June 2022, the Australian Bureau of Statistics reported that Australia had 13.6 million people in employment. This means that the charity sector’s 1.42 million employees accounted for 10.5% of Australia’s workforce and was comparable to the number of employees in the construction industry (1.2 million) and retail trade industry (1.4 million), highlighting the significance of Australia’s charities to the national economy.

Australian employment by industry data is available on the Australian Bureau of Statistics website.

Despite the challenges presented by COVID-19 in 2021, charities reported an increase of 40,000 employees across part-time, full-time and casual employees over the previous year and an increase of 111,000 over three years since 2018 when charities reported 1.31 million paid employees.

Table 10: Type of employment by charity size

| Size | Full-time | Part-time | Casual | |||

|---|---|---|---|---|---|---|

| % of total staff | Change | % of total staff | Change | % of total staff | Change | |

| Extra small | 29.4 | -6.8 | 30.9 | +0.1 | 39.6 | +6.7 |

| Small | 16.9 | -5.8 | 37.4 | -2.0 | 45.7 | +7.8 |

| Medium | 20.7 | -1.0 | 43.7 | +1.0 | 35.7 | +0.1 |

| Large | 32.9 | +0.6 | 38.0 | -2.9 | 29.1 | +2.3 |

| Very large | 39.9 | -0.7 | 36.6 | 0.1 | 23.5 | +0.8 |

| Extra large | 39.6 | +0.8 | 36.5 | +2.1 | 23.9 | -3.0 |

| Size unknown (BRC) | 33.0 | +0.2 | 46.0 | +2.0 | 21.0 | -2.3 |

| All charities | 37.7 | +0.2 | 37.1 | +0.5 | 25.2 | -0.6 |

Decreases in the percentage of full-time employees for extra small and small charities corresponded with similar increases in the percentage of casual employees for those charities.

Table 11: Number of employees by charity size

| Size | Full-time | Part-time | Casual | |||

|---|---|---|---|---|---|---|

| Number | Change | Number | Change | Number | Change | |

| Extra small | 3,249 | -1,891 | 3,416 | -950 | 4,378 | -298 |

| Small | 2,478 | -1,735 | 5,479 | -1,822 | 6,708 | -329 |

| Medium | 8,439 | -682 | 17,852 | -122 | 14,568 | -407 |

| Large | 72,795 | +2,085 | 83,906 | -5,418 | 64,338 | +5,742 |

| Very large | 188,037 | -1,957 | 172,766 | +1,063 | 110,683 | +4,618 |

| Extra large | 255,599 | +22,004 | 235,876 | +28,610 | 154,773 | -7,593 |

| Size unknown (BRC) | 5,465 | -106 | 7,602 | +142 | 3,469 | -483 |

| All charities | 536,062 | +17,718 | 526,897 | +21,503 | 358,917 | +1,250 |

Employee and volunteer breakdown by charity size

Extra large charities reported the biggest drop in volunteer numbers, with approximately 21,000 fewer volunteers compared to the previous reporting period.

In the 2020 reporting period extra small charities reported the highest increase in the number of employees. However, this wasn’t the case for the 2021 reporting period, where this cohort of charities reported the largest decrease in employees (approximately 22%, or 3,100 employees).

Small charities also reported a large decrease in employees, approximately 3,900 employees – a decrease of 21% on the previous reporting period.

Large, very large and extra large charities reported an increase in employees, with extra large charities reporting an additional 43,000 employees compared to the previous reporting period.

Generally, the ratio of volunteers to employees decreased as the size of the charity increased. Smaller charities and Basic Religious Charities were more reliant on volunteers while larger charities had more paid staff to deliver services.

Table 12: Employee and volunteer numbers by charity size with changes from the previous reporting periods

| Charity size | Volunteers | Employees | Volunteers per employee | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Number | % change from previous year | % change over 3 years | Number | % change from previous year | % change over 3 years | Ratio | % change | % change over 3 years | |

| Extra small | 228,604 | -8.8 | -18.2 | 11,043 | -22.1 | +37.4 | 20.7 | +17.2 | -40.4 |

| Small | 347,065 | +2.8 | +0.7 | 14,665 | -20.9 | -0.7 | 23.7 | +30.0 | +1.4 |

| Medium | 398,776 | -9.7 | -23.9 | 40,859 | -2.9 | -8.8 | 9.8 | -7.0 | -16.5 |

| Large | 1,226,051 | -5.5 | -11.0 | 221,039 | +1.1 | -2.0 | 5.5 | -6.5 | -9.2 |

| Very large | 547,202 | -3.3 | -1.3 | 471,486 | +0.8 | +8.1 | 1.2 | -4.0 | -8.7 |

| Extra large | 152,876 | -12.0 | -24.6 | 646,248 | +7.1 | +14.8 | 0.2 | -17.8 | -34.3 |

| Size unknown (BRC) | 276,080 | -5.9 | -43.6 | 16,536 | -2.6 | -7.9 | 16.7 | -3.3 | -38.7 |

| All charities | 3,176,654 | -5.5 | -15.8 | 1,421,876 | +2.9 | +8.5 | 2.2 | -8.2 | -22.4 |

Note: Charities report employee numbers based on their last pay period before submitting the Annual Information Statement. Volunteer numbers are based on the entire reporting period.

Highest total employees in Australia

Table 13: Charities with the most employees in Australia

| Charity name | Registered state | Subtypes | Staff – full time | Staff – part time | Staff – casual | Total employees |

|---|---|---|---|---|---|---|

| Melbourne Archdiocese Catholic Schools Ltd | VIC |

|

8,009 | 8,047 | 1,166 | 17,222 |

| UnitingCare QLD Group | QLD |

|

3,791 | 9,757 | 3,373 | 16,921 |

| Goodstart Early Learning Group | Not specified |

|

8,948 | 3,478 | 1,212 | 13,638 |

| Catholic Education Western Australia Limited | WA |

|

5,239 | 4,301 | 3,545 | 13,085 |

| St John Of God Health Care Inc | WA |

|

2,351 | 7,334 | 2,902 | 12,587 |

| Little Company of Mary Health Care Limited Group | VIC |

|

3,324 | 5,999 | 2,922 | 12,245 |

| Queensland University of Technology | QLD |

|

3,221 | 1,502 | 7,455 | 12,178 |

| University of Melbourne Group | VIC |

|

6,320 | 2,920 | 2,720 | 11,960 |

| The Corporation of The Trustees of The Roman Catholic Archdiocese of Brisbane | QLD |

|

5,703 | 4,292 | 1,828 | 11,823 |

| University of NSW Group | NSW |

|

5.608 | 1,225 | 4,323 | 11,156 |

Note: Some charities have permission from the ACNC to report as part of a group.

See page 44 of PDF for details about subtypes.

Highest number of volunteers in Australia

Table 14: Charities with the highest number of volunteers in Australia

| Charity name | Registered state | Subtype categories | Total volunteers |

|---|---|---|---|

| Clean Up Australia Limited | NSW |

|

745,694 |

| Surf Life Saving New South Wales Group | NSW |

|

74,937 |

| Surf Life Saving Australia Limited | NSW |

|

45,205 |

| Multiple Sclerosis Research Australia Limited | NSW |

|

40,000 |

| Surf Life Saving Queensland | QLD |

|

36,267 |

| PADI AWARE Group | VIC |

|

36,000 |

| Life Saving Victoria Limited | VIC |

|

25,000 |

| Surf Life Saving Western Australia Inc | WA |

|

24,473 |

| MATES in Construction (Aust) Limited | QLD |

|

23,473 |

| Surf Life Saving Sydney Northern Beaches Inc | NSW |

|

19,000 |

Note: See page 44 of the PDF for information about subtypes.

Table 15: Operating charities with no employees by charity size

| Charity size | % of operating charities with no employees |

|---|---|

| Extra small | 88.3 |

| Small | 53.9 |

| Medium | 22.9 |

| Large | 11.2 |

| Very large | 4.5 |

| Extra large | 3.7 |

| Size unknown (BRC) | 47.1 |

| Total | 50.0 |

Extra small, small charities and Basic Religious Charities were the most likely to operate without any paid staff.

To find out more about the people that work or volunteer for charities, visit our Charity Data Explorer.

Australia’s charities reported a significant increase in total revenue, expenses and assets in the 2021 reporting period.

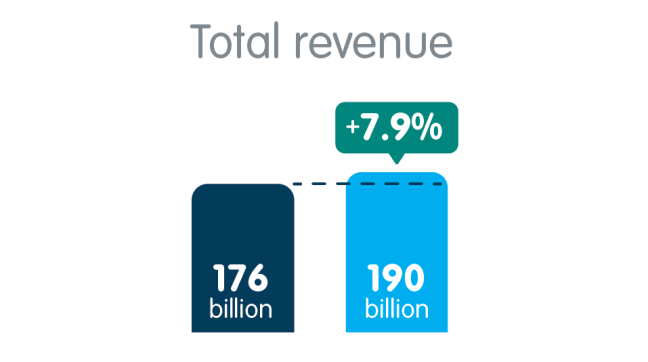

Charities generated approximately $190 billion in revenue – an increase of nearly $14 billion from the previous reporting period, and an increase of $34.5 billion from the $155.4 billion reported three years earlier.

However, expenses also increased by $7.1 billion from the previous reporting period.

Charities also reported more than $422 billion in assets, an increase of nearly $31 billion from the previous reporting period.

JobKeeper Payment Scheme

The JobKeeper Payment scheme was introduced during the pandemic to support Australian businesses and not-for-profits significantly impacted by COVID-19. JobKeeper commenced on 30 March 2020 and ended on 28 March 2021.

Information provided by the Australian Taxation Office (ATO) shows around 12,000 ACNC-registered charities received JobKeeper payments totalling around $7.6 billion. This included approximately $2.9 billion of payments in the 2019-2020 financial year, and around $4.7 billion in the 2020-2021 financial year.

JobKeeper payments to ACNC-registered charities supported an estimated 331,000 people in the period between April 2020 to September 2020. This fell to around 128,000 people in the period between October 2020 to December 2020, and to around 86,000 people between January 2021 to March 2021.

Income and expenses

Revenue and income

Revenue forms part of a charity’s income and relates to the funds a charity receives when undertaking its ordinary activities. Other income is income (or a loss) from transactions that are not part of a charity’s ordinary activities but affect the charity’s profit or loss. Other income can include a realised gain or loss on the sale of assets of the charity or changes (positive or negative) in the value of a charity’s currently held investments. A charity’s total income is made up of its total revenue and other income.

Total revenue increased in the 2021 reporting period, rising by nearly $14 billion (7.9%) on the previous reporting period to a total of $190 billion.

For context, the Australian Bureau of Statistics reported the Australian economy grew by 3.6% in the 2021–22 financial year.

While total revenue across the sector increased, this was not the case for all charity sizes. Only medium, very large and extra large charities reported an increase in total revenue.

Data from the 2021 Annual Information Statement shows that the largest charities continue to account for most of the sector’s aggregate revenue. Extra large charities, which make up 0.5% of Australia’s charity sector, accounted for more than 50% of the sector’s aggregate revenue.

Extra small charities, despite making up approximately one-third of the sector, contributed 0.1% of the aggregate revenue.

Table 16: Total revenue by charity size with changes from the previous reporting periods

| Size | Total revenue ($ million) |

Contribution to the sector’s total revenue (%) | Change from previous period ($ million) |

% change from previous period | Change from 2018 Charities Report ($ million) |

% change over 3 years |

|---|---|---|---|---|---|---|

| Extra small | 215 | 0.1 | -5 | -2.4 | -3 | -1.5 |

| Small | 1,281 | 0.7 | -16 | -1.2 | -4 | -0.3 |

| Medium | 3,635 | 1.9 | +108 | +3.1 | +123 | +3.5 |

| Large | 21,883 | 11.5 | -53 | -2.4 | +37 | +0.2 |

| Very large | 60,168 | 31.7 | +2,477 | +4.3 | +9,077 | +17.8 |

| Extra large | 102,798 | 54.1 | +11.954 | +13.2 | +25,308 | +32.7 |

| All charities | 189,981 | 100.0 | +13,982 | +7.9 | +34,538 | +22.2 |

Total income in the 2021 reporting period increased by more than $18 billion on the previous year to $196 billion, and by $37.5 billion on the figure reported by charities three years earlier in the 2018 Australian Charities Report.

Other income of nearly $6 billion, an increase of over $4 billion from the previous reporting period, formed a significant part of the increase in total income.

The increase in total income was mainly driven by larger charities.

Table 17: Total income by charity size with changes from the previous reporting periods

| Size | Total income ($ million) |

Change from previous period ($ million) |

% change from previous period | Change from 2018 Charities Report ($ million) |

% change over 3 years |

|---|---|---|---|---|---|

| Extra small | 297 | +43 | +16.9 | +20 | +7.1 |

| Small | 1,470 | +143 | +10.7 | +105 | +7.7 |

| Medium | 4,092 | +570 | +16.2 | +442 | +12.1 |

| Large | 23,181 | +495 | +2.2 | +436 | +1.9 |

| Very large | 62,078 | +3,791 | +6.5 | +10,007 | +19.2 |

| Extra large | 104,841 | +13,144 | +14.3 | +26,485 | +33.8 |

| All charities | 195,959 | +18,186 | +10.2 | +37,495 | +23.7 |

The 10 largest charities by revenue (which includes charities that report collectively to the ACNC as part of reporting groups) accounted for 13% of the sector’s revenue, and the 50 largest charities accounted for 33%.

Table 18: Largest charities by revenue in Australia

| Charity name | Registered state | Total revenue $ |

|---|---|---|

| The University of Sydney | NSW | 3,198,720,658 |

| University of Melbourne Group | VIC | 3,163,445,000 |

| Catholic Education Commission of Victoria Limited | VIC | 3,079,226,256 |

| Monash University | VIC | 2,879,192,943 |

| St Vincent’s Health Australia Ltd | NSW | 2,835,505,999 |

| The University of Queensland Group | QLD | 2,435,140,000 |

| St John Of God Health Care Inc | WA | 2,019,946,000 |

| Melbourne Archdiocese Catholic Schools Ltd | VIC | 2,005,603,779 |

| UnitingCare QLD Group | QLD | 1,704,514,000 |

| Little Company of Mary Health Care Limited Group | VIC | 1,534,429,000 |

A further breakdown of Australia’s largest charities by state can be found in Appendix 1.

Expenses

Registered charities must use their funds to further their charitable purpose or purposes. For some charities, part of their income and/or assets may be required to be applied to specific charitable outcomes (such as a specific bequest). The cost of running a charity is also impacted by inflation, with the Consumer Price Index rising 3.8% over the 12 months to the June 2021 quarter.

The charity sector’s total expenses increased by $7.1 billion to $174.8 billion in the 2021 reporting period. This increase is lower than the $10.2 billion increase reported in the previous reporting period. Three years earlier in the 2018 reporting period, total expenses were reported to be $148.5 billion.

The increase in expenses over the previous year (4.2%) was less than the increase in revenue (7.9%) in the 2021 reporting period. In the 2020 reporting period the increase in expenses (6.4%) was greater than the increase in revenue (6%).

Table 19: Total expenses by charity size with changes from the previous reporting periods

| Size | Total expenses ($ million) | Change from previous period ($ million) |

% change from previous period | Change over 3 years ($ million) |

% change over 3 years |

|---|---|---|---|---|---|

| Extra small | 385 | +15 | +4.2 | +39 | +11.4 |

| Small | 1,228 | -174 | -12.4 | -15 | -1.2 |

| Medium | 4,223 | +920 | +27.8 | +631 | +17.6 |

| Large | 19,875 | -893 | -4.3 | -594 | -2.9 |

| Very large | 54,948 | +1,252 | +2.3 | +7,198 | +15.1 |

| Extra large | 94,213 | +5,952 | +6.7 | +19,088 | +25.4 |

| All charities | 174,873 | +7,073 | +4.2 | +26,347 | +17.7 |

Net income

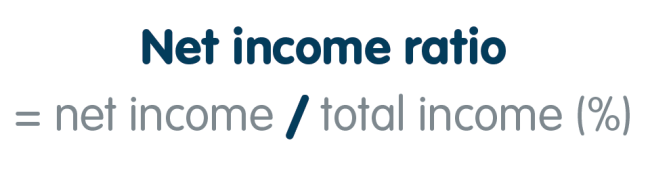

Net income is measured by subtracting a charity’s total expenses from its total income.

In the 2021 reporting period, the sector’s net income was reported as $21 billion, an increase of $11 billion compared to the previous reporting period. Net income was also significantly higher than the $9.9 billion reported three years earlier.

Compared to the previous reporting period, large, very large and extra large charities reported an increase in net income.

Increases in government revenue, investment revenue and other income as well as a much lower increase in charity expenses all contributed to the increase in net income.

Table 20: Net income by charity size with changes from the previous reporting periods

| Size | Net income ($ million) | Change from previous period ($ million) | % change from previous period | Change over 3 years ($ million) | % change over 3 years |

|---|---|---|---|---|---|

| Extra small | -88 | +26 | +22.9 | -19 | -28.5 |

| Small | 242 | +316 | +422.6 | +120 | +98.7 |

| Medium | -130 | -349 | -159.5 | -189 | -323.7 |

| Large | 3,306 | +1,388 | +72.4 | +1,031 | +45.3 |

| Very large | 7,130 | +2,539 | +55.3 | +2,810 | +65.0 |

| Extra large | 10,520 | +7,084 | +206.2 | +7,289 | +225.6 |

| All charities | 20,979 | +11,005 | +110.3 | +11,041 | +111.1 |

Assets and liabilities

Total assets

In the 2021 reporting period, the value of charities’ total assets increased by approximately $31 billion (7.9%).

As a result, total assets in the sector were approximately $422 billion. The value of the charity sector’s total assets in the 2018 reporting period was $323.3 billion.

Very large and extra large charities were mostly responsible for the increase in assets, with reported increases of $11.3 billion and $14.6 billion respectively compared to the previous reporting period.

Table 21: Total assets by charity size with changes from the previous reporting periods

| Charity size | Total assets ($ million) | Change from previous period ($ million) | % change from previous period | Change over 3 years ($ million) | % change over 3 years |

|---|---|---|---|---|---|

| Extra small | 4,266 | +656 | +18.2 | +1,305 | +44.1 |

| Small | 8,301 | -785 | -8.6 | -1,306 | -13.6 |

| Medium | 17,973 | +1,482 | +9.0 | +3,835 | +27.1 |

| Large | 58,775 | +3,419 | +6.2 | +8,455 | +16.8 |

| Very Large | 131,417 | +11,288 | +9.4 | +24,784 | +23.2 |

| Extra large | 201,388 | +14,682 | +7.9 | +61,711 | +44.2 |

| All charities | 422,120 | +30,742 | +7.9 | +98,785 | +30.6 |

Note: Assets include anything of commercial value that is controlled by a charity — examples of assets include cash and cash equivalents, shares, property, plant and equipment and trademarks.

Total liabilities

Total liabilities for charities increased by approximately $4.1 billion (3.0%) to $141.7 billion in the 2021 reporting period. This figure represented an increase in liabilities of approximately $40.6 billion (40.2%) compared to three years earlier. Total liabilities in the sector have been increasing since the 2016 reporting period, when charities reported liabilities of $87 billion.

Table 22: Total liabilities by charity size with changes from the previous reporting periods

| Charity size | Total liabilities ($ million) | Change from previous period ($ million) | % change from previous period | Change over 3 years ($ million) | % change over 3 years |

|---|---|---|---|---|---|

| Extra small | 504 | -144 | -22.2 | +34 | +7.1 |

| Small | 979 | -79 | -7.5 | -1,743 | -64.0 |

| Medium | 2,157 | +228 | +11.8 | +304 | +16.4 |

| Large | 13,887 | +668 | +5.0 | +2,155 | +18.4 |

| Very large | 45,719 | +1,092 | +2.4 | +10,222 | +28.8 |

| Extra large | 78,453 | +2,370 | +3.1 | +29,642 | +60.7 |

| All charities | 141,699 | +4,135 | +3.0 | +40,613 | +40.2 |

Note: Liabilities are generally defined as what a charity owes. They include anything of commercial value that is owed by a charity — such as bank overdrafts, amounts owed to suppliers or creditors, loans and employee entitlements.

Net assets/liabilities and the asset ratio

Overall, the increase in assets for charities in the 2021 reporting period was greater than the increase in liabilities.

The charity sector reported net assets of approximately $281 billion, an increase of $26.7 billion over the 2020 reporting period. This compares to an increase of $13.8 billion reported in the 2020 reporting period. Charities reported $222.2 billion in net assets three years earlier.

On average, charities continued to hold more assets than liabilities in the 2021 reporting period. The asset ratio provides the ratio of a charity’s assets to its liabilities.

A ratio of more than one indicates that a charity’s assets exceed its liabilities.

The higher the ratio, the greater the difference between assets and liabilities. And a higher asset ratio can indicate that a charity has set aside funds – known as reserves – to help ensure its financial stability and sustainability.

Overall, charities held three times more in assets than liabilities. This represents an increase in the asset ratio of 2.8 from the previous reporting period, but a decrease in the asset ratio of three years ago (3.2).

Table 23: Net asset/liabilities by charity size with changes from the previous reporting periods

| Charity size | Net assets / liabilities ($ million) | % change from previous period | % change over 3 years | Asset ratio (average) | Change from previous period asset ratio | Change to asset ratio over 3 years |

|---|---|---|---|---|---|---|

| Extra small | 3,826 | +29.2 | +53.7 | 8.5 | +2.9 | +2.2 |

| Small | 7,321 | -8.8 | +6.4 | 8.5 | -0.1 | +4.9 |

| Medium | 15,817 | +8.6 | +28.7 | 8.3 | -0.2 | +0.7 |

| Large | 44,887 | +6.5 | +16.3 | 4.2 | <+0.1 | -0.1 |

| Very large | 85,699 | +13.5 | +20.5 | 2.9 | +0.2 | -0.1 |

| Extra large | 122,935 | +11.1 | +35.3 | 2.6 | +0.1 | -0.3 |

| All charities | 281,239 | +10.5 | +26.2 | 3.0 | +0.1 | -0.2 |

Charities generate revenue from a range of sources, and it differs according to charity size and purposes. The larger the charity, the more likely it was to have revenue from multiple sources.

Government contributed more than half of the total revenue for charities, which was similar to 2020.

This section includes financial information from 41,659 charities, including Basic Religious Charities that voluntarily reported finances, as well as charities that did not report activities in the 2021 Annual Information Statement, but who did report on their finances.

Revenue sources

The revenue sources that a charity must report depend on its size.

Table 24: Revenue reporting requirements based on charity size

| Are charities required to provide this information in the Annual Information Statement? | ||

|---|---|---|

| Revenue source | Extra small and small charities (revenue under $250,000) | Medium to extra large charities (revenue of $250,000 or more) |

| Revenue from government (including grants) | Yes | Yes |

| Revenue from donations and bequests | Yes | Yes |

| Revenue from goods and services | No — optional | Yes |

| Revenue from investments | No — optional | Yes |

| Other revenue | Yes | Yes |

Note: Revenue from government also includes revenue received under a contract with government to provide specific services.

Breakdown of charity revenue sources

In the 2021 reporting period, revenue from government was $97.2 billion, an increase of nearly $8.5 billion from the previous reporting period.

Revenue from goods or services increased by nearly $2 billion, while revenue from investments increased by $1.4 billion compared to the previous reporting period.

Overall, donations rose by 5.3% to $13.4 billion, compared to an 8% increase in the previous reporting period. Donations increased by 27.2% from the 2018 reporting period figures, when revenue from donations was $10.5 billion.

There was a significant increase in total revenue from investments (28.5%) compared to the 2020 reporting period, where total revenue from investments decreased by 15.3%. These changes can likely be explained by the impacts of COVID-19 which resulted in a significant decline in financial markets in the 2020 reporting period, followed by a recovery in financial markets in the 2021 reporting period.

Revenue from government, donations and bequests, and investments all increased by more than 25% compared to figures reported in the 2018 reporting period.

The top 10 charities by donation and bequest revenue (including charities that report collectively as groups) contributed to nearly 18% of the sector’s total donations or bequests.

Table 25: Revenue source by charity size with changes from the previous reporting periods

| Charity size | Extra small | Small | Medium | Large | Very large | Extra large | All charities | |

|---|---|---|---|---|---|---|---|---|

| Government (including grants) | $ million | 24 | 212 | 1,183 | 9,855 | 29,231 | 56,742 | 97,247 |

| % change | +3.5 | -2.1 | +1.7 | -10.8 | +2.5 | +18.7 | +9.5 | |

| % change over 3 years | +35.2 | +28.6 | +17.4 | -4.4 | +23.8 | +47.2 | +32.0 | |

| Donations and bequests | $ million | 84 | 513 | 1,022 | 3,266 | 4,625 | 3,849 | 13,360 |

| % change | -0.3 | +2.1 | +4.4 | +7.7 | +1.5 | +9.1 | +5.3 | |

| % change over 3 years | +1.1 | +6.6 | +10.7 | +15.6 | +7.3 | +104.9 | +27.2 | |

| Goods or services | $ million | 46 | 279 | 832 | 6,215 | 21,259 | 30,599 | 59,229 |

| % change | -1.1 | +2.6 | +6.0 | +4.4 | +5.5 | +1.9 | +3.5 | |

| % change over 3 years | +1.0 | -7.4 | -11.6 | +1.3 | +15.6 | +11.7 | +11.3 | |

| Investments | $ million | 32 | 124 | 289 | 1,080 | 1,798 | 3,080 | 6,404 |

| % change | -13.1 | -16.7 | +2.6 | +24.8 | +46.6 | +27.1 | +28.5 | |

| % change over 3 years | -9.1 | -18.4 | -1.7 | +9.7 | +26.5 | +139.6 | +53.5 | |

| Other revenue | $ million | 29 | 153 | 309 | 1,467 | 3,256 | 8,527 | 13,741 |

| % change | -1.7 | -2.4 | -2.7 | -3.4 | +0.6 | +20.9 | +11.6 | |

| % change over 3 years | -20.7 | -17.7 | -10.9 | -7.8 | -3.3 | +1.8 | -1.2 |

Except for extra small and extra large charities, the proportion of revenue charities received from government decreased in comparison to the previous reporting period.

Extra small charities received the least revenue from government, and generally speaking, the percentage of revenue that came from government increased with charity size.

Donations and bequests comprised just under 4% of extra large charities’ total revenue. In comparison, this revenue source comprised more than 39% of extra small charities’ total revenue.

Table 26: Revenue sources as a percentage of total revenue by charity size with changes from the previous reporting periods

| Charity size | Extra small | Small | Medium | Large | Very large | Extra large | All charities | |

|---|---|---|---|---|---|---|---|---|

| Government (including grants) | % | 11.1 | 16.5 | 32.5 | 45.0 | 48.6 | 55.2 | 51.2 |

| % change | +0.6 | -0.1 | -0.4 | -4.2 | -0.9 | +2.6 | +0.7 | |

| % change over 3 years | +3.0 | +3.7 | +3.8 | -2.2 | +2.4 | +5.4 | +3.8 | |

| Donations and bequests | % | 39.1 | 40.1 | 28.1 | 14.9 | 7.7 | 3.7 | 7.0 |

| % change | +0.8 | +1.3 | +0.4 | +1.4 | -0.2 | -0.1 | -0.2 | |

| % change over 3 years | +1.0 | +2.6 | +1.8 | +2.0 | -0.7 | +1.3 | +0.3 | |

| Goods or services | % | 21.2 | 21.8 | 22.9 | 28.4 | 35.3 | 29.8 | 31.2 |

| % change | +0.3 | +0.8 | +0.6 | +1.8 | +0.4 | -3.3 | -1.3 | |

| % change over 3 years | +0.5 | -1.6 | -3.9 | +0.3 | -0.7 | -5.5 | -3.1 | |

| Investments | % | 15.0 | 9.7 | 8.0 | 4.9 | 3.0 | 3.0 | 3.4 |

| % change | -1.8 | -1.8 | -0.04 | +1.1 | +0.9 | +0.3 | +0.5 | |

| % change over 3 years | -1.2 | -2.1 | -0.4 | +0.4 | +0.2 | +1.3 | +0.7 | |

| Other revenue | % | 13.6 | 11.9 | 8.5 | 6.7 | 5.4 | 8.3 | 7.2 |

| % change | +0.1 | -0.1 | -0.5 | -0.1 | -0.2 | +0.5 | +0.2 | |

| % change over 3 years | -3.2 | -2.6 | -1.4 | -0.6 | -1.2 | -2.5 | -1.7 |

Revenue sources reported by charities

In the 2021 reporting period, 45.4% of charities reported receiving revenue from government. That figure represented a 1.5% decrease from the previous reporting period but was close to a 9% increase on the figure recorded in the 2018 reporting period.

15.4% of extra small charities reported receiving revenue from government (a marginal decrease from 15.7% in the previous reporting period), whereas more than 94% of extra large charities reported receiving revenue from government, a figure similar to the previous reporting period.

Fewer medium charities reported revenue from government in the 2021 reporting period (67.5% compared to 70% in 2020). However, the 2021 figure was up almost 16% on that recorded in the 2018 reporting period.

Despite an increase in the total revenue charities received from donations, the percentage of charities that reported receiving revenue from donations or bequests (66.2%) remained stable in the 2021 reporting period and was similar to the percentage recorded in the 2018 reporting period (65.9%).

With the exception of a slight increase for extra large charities, the percentage of charities reporting revenue from investments (55%) decreased compared to the previous reporting period (58.2%).

And outside of extra large and very large charities, the percentage of charities with revenue from investments has also decreased over the past three years.

Table 27: Percentage of charities that reported revenue from different sources by size with changes from previous reporting periods

| Charity size | Extra small | Small | Medium | Large | Very large | Extra large | All charities | |

|---|---|---|---|---|---|---|---|---|

| Government (including grants) | % of total revenue | 15.4 | 42.4 | 67.5 | 80.2 | 91.2 | 94.3 | 45.4 |

| % change | -0.4 | -1.3 | -2.5 | -3.7 | -1.9 | +0.5 | -1.5 | |

| % change over 3 years | +1.5 | +15.9 | +16.1 | +8.8 | +4.6 | +0.9 | +8.9 | |

| Donations and bequests | % of total revenue | 54.7 | 74.8 | 73.8 | 70.6 | 69.7 | 79.1 | 66.2 |

| % change | -1.3 | +1 | - | -0.7 | -0.7 | -5.2 | -0.4 | |

| % change over 3 years | -0.7 | +2.7 | +2.3 | -1.2 | -1.5 | -0.9 | +0.3 | |

| Goods or services | % of total revenue | 30.7 | 48.7 | 64.6 | 77.1 | 86.8 | 86.9 | 51.4 |

| % change | -1.1 | +0.02 | -0.8 | -2.3 | -0.7 | -3.1 | -0.9 | |

| % change over 3 years | +0.4 | +0.9 | +0.03 | -0.5 | +1.6 | -0.4 | +0.4 | |

| Investments | % of total revenue | 40.1 | 50.3 | 63.9 | 76.3 | 84.9 | 91.0 | 55.0 |

| % change | -2.4 | -5 | -4.3 | -2.2 | -1.5 | +0.1 | -3.2 | |

| % change over 3 years | -0.9 | -3.1 | -4.5 | -2.1 | +0.8 | +3.2 | -2.1 | |

| Other revenue | % of total revenue | 35.8 | 48.2 | 60.9 | 73.7 | 84.2 | 87.3 | 51.9 |

| % change | -1.1 | -2.4 | -0.9 | -2.9 | -1.1 | -1.2 | -1.6 | |

| % change over 3 years | -2.4 | -5.2 | -0.6 | -1.8 | +1.6 | -4.4 | -2.5 |

Charities must use funds to further their charitable purposes, and some assets held by charities may have additional conditions on how they can be used – for example, some grants or gifts must be used for specific purposes.

Charities are a significant employer in Australia, with more than half of the sector’s expenses being employee expenses. Charities also distributed nearly $10 billion on grants and donations in the 2021 reporting period.

Types of expenses

The expenses that a charity must report to the ACNC are based on its size. In the Annual Information Statement all charities must report the following expenses:

- Employee

- Grants and donations within Australia

- Grants and donations outside Australia

- Other (for example, rental expenses, bank charges, utilities)

- Large, very large and extra large charities must also report interest expenses.

Employee expenses

According to 2021 reporting period figures, charities spent nearly $99 billion on employee expenses – a 5.4% increase on the previous reporting period. The increases were seen mostly in the expenses of very large and extra large charities.

This reflects the 40,000 increase in charity employees to 1.42 million employees in the 2021 reporting period. In the 2018 reporting period, employee expenses were $81 billion.

Table 28: Employee expenses by charity size with changes from the previous reporting periods

| Charity size | Employee expenses | ||||

|---|---|---|---|---|---|

| $ million | Change over previous year ($ million) | % change | Change over 3 years ($ million) | % change over 3 years | |

| Extra small | 33 | +2 | +6.4 | +4 | +13.4 |

| Small | 305 | -4 | -1.2 | +4 | +1.4 |

| Medium | 1,864 | +471 | +33.8 | +445 | +31.4 |

| Large | 10,851 | -777 | -6.7 | -346 | -3.1 |

| Very large | 32,119 | +783 | +2.5 | +5,210 | +19.4 |

| Extra large | 53,632 | +4,614 | +9.4 | +12,411 | +30.1 |

| All charities | 98,804 | +5,089 | +5.4 | +17,728 | +21.9 |

Interest and other expenses

‘Interest expenses’ details the interest paid by charities on any money they have borrowed. Only large, very large and extra large charities are required to report on interest expenses.

‘Other expenses’ includes all expenses other than employee expenses, and grants and donations made in and outside Australia. For extra small, small and medium charities, interest expenses are included within ‘Other expenses’.

Other expenses may include expenses such as rent, insurance, bank charges, consultancy fees, cost of goods sold, equipment hire, depreciation, fundraising expenses, utilities and other administration.

In the 2021 reporting period, charities reported a $43 million decrease in interest expenses.

Interest and other expenses accounted for $60.3 billion in expenditure in the 2018 reporting period, where they comprised $982 million in interest expenses and $59.3 billion in other expenses.

Table 29: Interest and other expenses by charity size with changes from the previous reporting periods

| Charity size | Interest expenses | Other expenses | ||||

|---|---|---|---|---|---|---|

| $ million | % change | % change over 3 years | $ million | % change | % change over 3 years | |

| Extra small | - | - | - | 189 | -5.3 | -8.9 |

| Small | - | - | - | 622 | -18.0 | -5.2 |

| Medium | - | - | - | 1,839 | +38.2 | +7.9 |

| Large | 118 | -28.6 | -21.1 | 6,842 | -5.2 | -9.5 |

| Very large | 452 | -9.2 | +28.2 | 19,181 | +0.4 | +6.4 |

| Extra large | 908 | +5.8 | +89.4 | 36,208 | +4.3 | +16.2 |

| All charities | 1,478 | -2.8 | +50.6 | 64,880 | +2.5 | +9.4 |

Note: Extra small, small and medium charities do not separately report interest expenses in the Annual Information Statement.

Breakdown of types of charity expenses

Overall, the employee expenses that charities reported in the 2021 reporting period accounted for 56.5% of total charity expenses compared to 55.8% of total charity expenses in the 2018 reporting period.

The percentage of expenses charities spent on employees was higher for larger charities.

Extra small charities reported more than 8% of expenses going to employee costs, whereas the three large categories all reported 54% or more of expenses going to employee costs.

To find out more about charity revenue and expenditure visit our Charity Data Explorer.

Table 30: Charity expenses as a percentage of total expenses by charity size with changes from the previous reporting periods

| Extra small | Small | Medium | Large | Very large | Extra large | All charities | ||

|---|---|---|---|---|---|---|---|---|

| Employee expenses | % of total expenses | 8.5 | 24.8 | 44.2 | 54.6 | 58.5 | 56.9 | 56.5 |

| % change | +0.2 | +2.8 | +2.0 | -1.4 | +0.1 | +1.4 | +0.7 | |

| % change over 3 years | +0.2 | +0.6 | +4.7 | -0.1 | +2.1 | +2.0 | +1.9 | |

| Interest expenses | % of total expenses | - | - | - | 0.6 | 0.8 | 1 | 0.8 |

| % change | - | - | - | -0.2 | -0.1 | -0.02 | -0.1 | |

| % change over 3 years | - | - | - | -0.1 | +0.1 | +0.4 | +0.1 | |

| Grants and donations within Australia | % of total expenses | 38 | 19.9 | 9.8 | 7.4 | 4.4 | 3 | 4.3 |

| % change | +4.5 | +0.4 | -5.0 | +0.6 | +0.5 | -0.4 | -0.1 | |

| % change over 3 years | +11.3 | +0.5 | -0.9 | +1.4 | +0.7 | +0.5 | +0.5 | |

| Grants and donations within Australia | % of total expenses | 4.6 | 4.7 | 2.5 | 3 | 1.4 | 0.7 | 1.3 |

| % change | +0.6 | +0.2 | -0.3 | +1.3 | +0.2 | -0.1 | +0.1 | |

| % change over 3 years | -0.5 | +1.0 | +0.1 | +1.4 | +0.03 | +0.2 | +0.3 | |

| Other expenses | % of total expenses | 49 | 50.6 | 43.5 | 34.4 | 34.9 | 38.4 | 37.1 |

| % change | -5.0 | -3.4 | +3.3 | -0.3 | -0.7 | -0.9 | -0.6 | |

| % change over 3 years | -10.9 | -2.1 | -3.9 | -2.5 | -2.9 | -3.1 | -2.8 |

Note: Extra small, small and medium charities do not separately report interest expenses in the Annual Information Statement.

The provision of grants, donations and structured philanthropy are important components of the charity sector.

Our data shows nearly a fifth of all charities are grant-makers of some type, including ancillary funds and other types of charitable trusts.

The Australian Government has pledged to work with the sector to double philanthropic giving by 2030.

In March 2023, the Government established a Productivity Commission review to analyse motivations for philanthropic giving in Australia and identify opportunities for growth.

This analysis aims to aid public understanding of giving and philanthropy in Australia.

Grant-making charities

There are a number of different types of grant-making charities including:

- Ancillary funds which are trusts established for the purpose of giving money, property or benefits to deductible gift recipients. There are two types of ancillary funds:

- Private ancillary funds (PAFs) are established for private philanthropy – for example, by family groups

- Public ancillary funds (PuAFs) collect donations from the public.

- 'Other types of trusts' which have been established to hold and distribute funds for charitable purposes.

For the purposes of this report, we adopted the term ‘structured philanthropy’ which was used in the ACNC's report Australia’s Grant-Making Charities in 2016. The term refers collectively to private ancillary funds, public ancillary funds and other types of trusts.

Structured philanthropy accounts for about 14% of all Australian charities.

For the fourth category of grant-making charities we use the term ‘other grant-makers’ in this report. These are charities that classified a program as grant-making or reported grants and donations expenses (in Australia or overseas) of more than 70% of their total expenses.

Other grant-makers account for just under 5% of all registered charities.

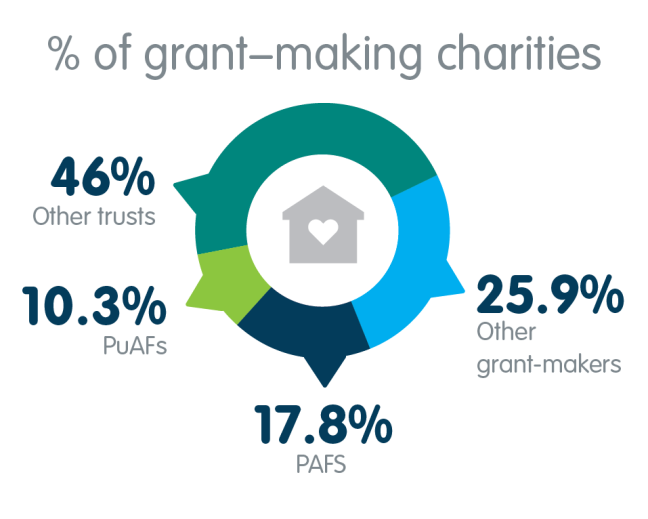

Of 11,427 grant-making charities, 8,467 (74.1%) were either private ancillary funds, public ancillary funds or other trusts (structured philanthropy). Charities classed as other grant-makers comprise 25.9% of Australia’s charities (2,960 charities).

Table 31: Summary of all grant-making charities as of 8 February 2023

| Category of grant-maker | Number of charities | % of grant-making charities | % of all charities |

|---|---|---|---|

| PAFs | 2,035 | 17.8 | 3.4 |

| PuAFs | 1,172 | 10.3 | 1.9 |

| Other trusts | 5,260 | 46.0 | 8.7 |

| All structured philanthropy (i.e. PAFs, PuAFs and trusts) | 8,467 | 74.1 | 14.0 |

| Other grant-makers | 2,960 | 25.9 | 4.9 |

| Total grant-makers | 11,427 | 100.0 | 19.0 |

Of the 11,427 grant-makers identified overall, 10,165 submitted an individual 2021 Annual Information Statement.

Those that did not submit an individual 2021 Annual Information Statement might have been members of an ACNC-approved reporting group, or were registered with the ACNC after the 2021 reporting period.

The number of other grant-makers in this year’s report cannot be compared directly to figures in the Australia’s Grant-making Charities in 2016 report. This is because the taxonomy charities use to report on their work and activities has changed.

The number of private ancillary funds and other trusts reporting increased by 32% and 13% respectively, but the number of public ancillary funds decreased by 19%. Statistics from the Australian Taxation Office show that the current number of endorsed public ancillary funds has declined since 2016, whereas the number of endorsed private ancillary funds has continued to increase.

Table 32: Summary of grant-making charities that submitted the 2021 Annual Information Statement

| Category of grant-maker | Number of charities | % of grant-making charities | % of all charities |

|---|---|---|---|

| PAFs | 1,735 | 17.1 | 3.5 |

| PuAFs | 986 | 9.7 | 2.0 |

| Other trusts | 4,640 | 45.6 | 9.4 |

| All structured philanthropy (i.e. PAFs, PuAFs and trusts) | 7,361 | 74.1 | 14.9 |

| Other grant-makers | 2,804 | 25.9 | 5.7 |

| Total grant-makers | 10,165 | 100.0 | 20.6 |

Private ancillary funds and public ancillary funds received almost all of their revenue from either donations and bequests, or investments. This contrasted with grant-makers classed as other trusts and other grant-makers, who received a far higher percentage of their total revenue from government.

Table 33: Grant-maker revenue sources as a percentage of total revenue

| PAFs | PuAFs | Other trusts | All structured philanthropy | Other grant-makers | Total grant-makers | |

|---|---|---|---|---|---|---|

| Government (including grants) % | <0.1 | 0.6 | 29.8 | 18.9 | 47.6 | 27.5 |

| Donations and bequests % | 69.1 | 68.3 | 21.5 | 38.9 | 39.4 | 39.0 |

| Goods or services % | 0.1 | 2.1 | 17.0 | 11.1 | 2.6 | 8.5 |

| Investments % | 27.2 | 26.2 | 15.3 | 19.5 | 4.7 | 15.1 |

| Other revenue % | 3.5 | 2.8 | 16.4 | 11.6 | 5.7 | 9.8 |

Grant-makers total assets amounted to approximately $51 billion. On average, grant-makers held $5 million in assets, with charities categorised as structured philanthropy holding an average of $6.06 million, compared to $2.35 million for other grant-makers.

Table 34: Grant-maker total and average assets

| Category of grant-maker | Number of charities | Average assets | Total assets $ |

|---|---|---|---|

| PAFs | 1,735 | 7,002,478 | 12,149,298,730 |

| PuAFs | 986 | 5,817,844 | 5,736,394,322 |

| Other trusts | 4,640 | 5,762,450 | 26,737,768,420 |

| All structured philanthropy (i.e. PAFs, PuAFs and trusts) | 7,361 | 6,062,147 | 44,623,461,472 |

| Other grant-makers | 2,804 | 2,347,737 | 6,583,055,587 |

| Total grant-makers | 10,165 | 5,037,532 | 51,206,517,059 |

More than 73% of grant-making charities’ total spending on grants and donations was for use in Australia with the remainder for use outside Australia. Spending on grants for use in Australia was significantly higher for charities categorised as structured philanthropy (90.6%) than it was for charities categorised as other grant-makers (61.8%).

Table 35: Grant-maker spending on grants and donations

| Grants and donations for use in Australia | Grants and donations for use in Australia | Total spending on grants and donations | ||||||

|---|---|---|---|---|---|---|---|---|

| Average $ | Total $ | % of total spending on grants | Average $ | Total $ | % of total spending on grants | Average $ | Total $ | |

| PAFs | 430,672 | 747,215,931 | 94.9 | 22,968 | 39,849,304 | 5.1 | 453,640 | 787,065,235 |

| PuAFs | 443,394 | 437,186,460 | 95.4 | 21,260 | 20,962,371 | 4.6 | 464,654 | 458,148,831 |

| Other trusts | 168,644 | 782,507,773 | 84.6 | 30,624 | 142,095,369 | 15.4 | 199,268 | 924,603,142 |

| All structured philanthropy | 267,207 | 1,966,910,164 | 90.6 | 27,565 | 202,907,044 | 9.4 | 294,772 | 2,169,817,208 |

| Other grant-makers | 741,483 | 2,079,118,032 | 61.8 | 458,912 | 1,286,788,317 | 38.2 | 1,200,395 | 3,365,906,349 |

| Total grant-makers | 398,035 | 4,046,028,196 | 73.1 | 146,551 | 1,489,695,361 | 26.9 | 544,587 | 5,535,723,557 |

Grants and donations

Some charities, such as ancillary funds and trusts, are primarily established to deliver structured philanthropy and focus solely on distributing grants and donations to other charities and charitable causes. For other charities, distributing grants and donations is only one element of their operations.

In the 2021 reporting period, charities reported spending $9.7 billion on grants and donations, an increase of 5% on the previous reporting period.

Of the $9.7 billion, charities spent $7.5 billion on grants and donations within Australia, an increase of $166 million (or 2.3%) compared to the previous reporting period. Grants and donations outside Australia rose by $298 million (or 15.8%) to $2.2 billion.

In the 2018 reporting period, $7.1 billion was spent on grants and donations – $5.6 billion within Australia and $1.5 billion outside Australia.

Total grants and donations have increased across all charity sizes over the past three years.

Table 36: Expenses on grants and donations by charity size, with changes from the previous reporting periods

| Charity size | Within Australia | Outside Australia | Total | ||||||

|---|---|---|---|---|---|---|---|---|---|

| $ million | % change | % change over 3 years | $ million | % change | % change over 3 years | $ million | % change | % change over 3 years | |

| Extra small | 146 | +18.3 | +58.3 | 18 | +21.0 | +0.6 | 164 | +18.6 | +49.1 |

| Small | 244 | -10.4 | +1.3 | 57 | -8.6 | +24.8 | 301 | -10.1 | +5.1 |

| Medium | 412 | -15.2 | +7.1 | 107 | +15.3 | +27.1 | 519 | -10.3 | +10.7 |

| Large | 1,461 | +4.2 | +18.1 | 603 | +68.5 | +84.4 | 2,064 | +17.3 | +32.0 |

| Very large | 2,413 | +14.5 | +34.8 | 783 | +20.1 | +17.7 | 3,196 | +15.8 | +30.2 |

| Extra large | 2,844 | -4.0 | +50.1 | 621 | -12.6 | +68.6 | 3,465 | -5.7 | +53.1 |

| All charities | 7,520 | +2.3 | +33.3 | 2,190 | +15.8 | +45.1 | 9,710 | +5.0 | +35.8 |

Table 37: Average expenses on grants and donations by charity size, with changes from the previous reporting periods

| Charity size | Within Australia | Outside Australia | Total | ||||||

|---|---|---|---|---|---|---|---|---|---|

| $ | % change | % change over 3 years | $ | % change | % change over 3 years | $ | % change | % change over 3 years | |

| Extra small | 9,378 | +17.0 | +49.1 | 1,140 | +19.7 | -5.2 | 10,518 | +17.3 | +40.4 |

| Small | 24,348 | -8.6 | +2.8 | 5,720 | -6.7 | +26.6 | 30,069 | -8.2 | +6.7 |

| Medium | 59,192 | -18.0 | +3.0 | 15,422 | +11.5 | +22.3 | 74,613 | -13.3 | +6.5 |

| Large | 220,083 | +5.6 | +15.3 | 90,872 | +70.8 | +80.0 | 310,955 | +18.9 | +28.9 |

| Very large | 1,094,287 | +10.2 | +19.0 | 355,253 | +15.6 | +3.9 | 1,449,540 | +11.5 | +14.9 |

| Extra large | 11,656,752 | -17.4 | +11.3 | 2,546,084 | -24.8 | +25.1 | 14,202,836 | -18.8 | +13.6 |

| All charities | 180,519 | +1.7 | +28.5 | 52,575 | +15.2 | +39.9 | 233,094 | +4.5 | +30.9 |

Donations and bequests by state and territory

In the 2021 reporting period, total donations and bequests revenue rose by more than $676 million from the previous reporting period to $13.4 billion. Overall, total donations and bequests revenue has increased by $2.9 billion since the 2018 reporting period.

Extra-large charities reported the largest increase in donation and bequests revenue – $322 million – in the 2021 reporting period. In total, these charities received $3.9 billion in donations and bequests revenue during this period. This is a 9% increase from the previous reporting period, and a 105% increase from the 2018 reporting period ($1.88 billion).

There has also been an increase in total donations and bequests to charities in every state and territory compared to the 2018 reporting period.

The largest increase was recorded by charities in Queensland, which saw a 66% (or $651 million) increase in donations and bequests revenue in comparison to the previous reporting period. Overall, Queensland charities have enjoyed a 54.8% (or $580 million) increase in donations and bequests revenue since the 2018 reporting period.

Conversely, Victorian charities recorded the smallest increase in donations and bequests revenue during the 2021 reporting period – up by only 0.2% (or $7 million) on 2020. However, the 2021 figure was still 19.8% ($493 million) higher than that recorded in the 2018 reporting period.

Table 38: Charity donations and bequests received by state and territory with changes from the previous reporting periods

| State or territory | Donations and bequests | ||||

|---|---|---|---|---|---|

| $ million | Change from previous period ($ million) | % change from previous period | Change from 2018 ($ million) | % change over 3 years | |

| ACT | 154 | +2 | +1.2 | +13 | +9.2 |

| NSW | 5,149 | +256 | +5.2 | +1,085 | +26.7 |

| NT | 27 | +4 | +15.6 | -4 | -12.4 |

| QLD | 1,639 | +651 | +66.0 | +580 | +54.8 |

| SA | 391 | +50 | +14.7 | +32 | +9.0 |

| TAS | 107 | +6 | +6.1 | +21 | +24.1 |

| VIC | 2,979 | +7 | +0.2 | +493 | +19.8 |

| WA | 657 | +53 | +8.9 | +180 | +37.8 |

Note: Charities that report as part of a group have been excluded from this analysis.

Approximately 41.5% of registered charities have deductible gift recipient (DGR) endorsement from the Australian Taxation Office. Organisations endorsed as deductible gift recipients are entitled to receive gifts which are deductible from the donor’s taxable income.

DGR-endorsed charities are more likely to receive donations.

To be DGR-endorsed, a charity must meet the specific criteria of a DGR category based on its purpose or purposes.

The 10 charities reporting the largest total donations and bequests revenue (including charities that report to the ACNC as part of reporting groups) accounted for approximately 18% of the sector’s total donations and bequests revenue.

A further breakdown of charities that received the largest total donations and bequests revenue by state and territory can be found in Appendix 2.

Table 39: 10 charities with highest donations and bequests received in current reporting period

| Charity name | Registered state | Subtype categories | Donations and bequests amount ($) |

|---|---|---|---|

| Asia Pacific Internet Development Trust | QLD |

|

590,173,475 |

| Minderoo Foundation Group | WA |

|

501,145,108 |

| Susan McKinnon Foundation | VIC |

|

330,512,170 |

| World Vision Australia | VIC |

|

288,604,000 |

| The Smith Family | NSW |

|

124,663,000 |

| Salvation Army – Social Work Group | VIC |

|

122,960,000 |

| Médecins Sans Frontières Australia Limited | NSW |

|

105,534,255 |

| L.D.S. Charitable Trust Fund | NSW |

|

99,474,019 |

| Compassion Australia | NSW |

|

94,550,578 |

| LDS Charities Australia | NSW |

|

93,000,000 |

Note: See page 44 of the PDF for information about subtypes.

A charity subtype is a category of registration that reflects a charity’s purposes.

Analysis of charity subtypes provides insights into the subsectors that make up the charity sector. We can learn more about the composition of these subsectors, the financial patterns within them, and how they compare with other subsectors.

The Australian Charities and Not-for-profits Commission Act 2012 (Cth) sets out 14 charity subtypes. These include the 12 charitable purposes set out in the Charities Act 2013 (Cth), as well as the categories of Public Benevolent Institution and Health Promotion Charity.

| Advancing health (health) | Advancing the security or safety of Australia or the Australian public (security) |

| Advancing education (education) | Preventing or relieving the suffering of animals (animals) |

| Advancing social or public welfare (social welfare) | Advancing the natural environment (environment) |

| Advancing religion (religion) | Any other purpose beneficial to the general public that may reasonably be regarded as analogous to, or within the spirit of, any of the purposes mentioned in the subtypes above (other) |

| Advancing culture (culture) | Promoting or opposing a change to any matter established by law, policy or practice in the Commonwealth, a state, a territory or another country (law) |

| Promoting reconciliation, mutual respect and tolerance between groups of individuals that are in Australia (reconciliation) | Public Benevolent Institution (PBI) |

| Promoting or protecting human rights (human rights) | Health Promotion Charity (HPC) |

Charities can be registered with multiple subtypes or can choose to not be registered with any subtype.

In addition to the 14 charity subtypes, our analysis includes two extra categories:

- charities registered with more than one subtype (for example, a charity with two subtypes is included in this category rather than in the two separate categories of its two subtypes)

- charities with no registered subtype.

Basic Religious Charities that did not provide financial information were not included in the subtype analysis. Charities that report as a group were also excluded from this data.

Approximately 30% of charities that submitted a 2021 Annual Information Statement were registered with more than one subtype. This compares to 23% in the 2018 reporting period.

The analysis of each subtype in this report is limited to charities registered solely with that single subtype. Consequently, the information from a charity with more than one subtype is not included in the analysis of each of its subtypes; it is included only in the category ‘Multiple’. Because of this, each subtype analysis in this report is not a complete picture of the subtype as a whole.

Table 40: Number of charities registered by subtype and charity size with changes from the previous reporting periods

| Subtype category | Extra small | Small | Medium | Large | Very large | Extra large | Total | ||

|---|---|---|---|---|---|---|---|---|---|

| Number | Change from previous year | Change from 3 years earlier | |||||||

| Health | 384 | 152 | 72 | 57 | 19 | 2 | 686 | +26 | +15 |

| Education | 2,107 | 1,267 | 1,116 | 1,029 | 492 | 52 | 6,063 | -21 | -193 |

| Social welfare | 732 | 350 | 238 | 160 | 19 | 1 | 1,500 | +50 | +85 |

| Religion | 1,916 | 2,381 | 1,102 | 415 | 44 | 6 | 5,864 | +140 | +544 |

| Culture | 718 | 292 | 229 | 171 | 26 | - | 1,436 | +73 | +228 |

| Recon-ciliation | 26 | 14 | 16 | 4 | - | - | 60 | +4 | +13 |

| Human rights | 16 | 13 | 4 | 4 | 1 | - | 38 | -1 | +2 |

| Security | 67 | 25 | 17 | 15 | - | - | 124 | +1 | -19 |

| Animals | 253 | 235 | 58 | 21 | 12 | - | 579 | +40 | +106 |

| Environ-ment | 311 | 162 | 132 | 83 | 18 | 2 | 708 | +62 | +111 |

| Other | 1,825 | 862 | 587 | 385 | 70 | 6 | 3,735 | +115 | +301 |

| Law | 15 | 5 | 3 | 4 | 2 | - | 29 | +1 | +5 |

| PBI | 611 | 455 | 535 | 925 | 382 | 31 | 2,939 | -113 | -207 |

| HPC | 156 | 68 | 71 | 95 | 42 | 1 | 433 | -9 | -22 |

| Multiple | 4,090 | 2,516 | 2,024 | 2,713 | 921 | 82 | 12,346 | +133 | +1,237 |

| No subtype | 2,354 | 1,199 | 725 | 474 | 67 | 5 | 4,824 | -305 | -730 |

Employees and volunteers by subtype

The number of employees and volunteers varied among charity subtypes.

Some charity subtypes were more likely to have employees delivering services while others were more likely to engage volunteers.

Table 41: Employees and volunteers by subtype with changes from the previous reporting periods

| Subtype category | Employees | Change over 1 year | Change over 3 years | Volunteers | Change over 1 year | Change over 3 years |

|---|---|---|---|---|---|---|

| Number | % | % | Number | % | % | |