Australia’s registered charities have an ongoing obligation to report annually to the ACNC. Charities do this by completing and submitting an Annual Information Statement (AIS) and, in the case of medium and large charities, an annual financial report (AFR).

This report looks at charities’ reporting during the 2017 reporting period.

As at 12 October 2018, charities had submitted 47,950 2017 AISs to the ACNC.

As shown in Figure 1 below, most charities are small and generally have lower levels of total assets and revenue.

In addition to an AIS, medium and large charities are required to submit an AFR to the ACNC.

To help us identify the type of AFR submitted to the ACNC, we improved the 2017 AIS so charities could select from the following types of financial statements:

- General purpose financial statements (GPFS)

- General purpose financial statements – Reduced Disclosure Requirements (GPFS – RDR)

- Special Purpose financial statements (SPFS)

Since 2015, the ACNC has reviewed the quality and accuracy of AISs and AFRs.

This has helped us:

- improve the quality and accuracy of information published on the ACNC Charity Register

- improve future iterations of the AIS

- identify any trends and errors in financial reporting

- improve guidance in financial reporting, and

- inform the ACNC when it considers any proposed changes to the financial reporting framework

We have also used our findings to reduce reporting errors charities make by introducing additional rules and validation to the AIS.

Improvements to the 2017 AIS allowed us to review more AFRs than in 2016. The bulk of this report is therefore focused on our review of AFRs.

What did we check for?

In 2017 we continued to review the financial information charities reported through the AIS, with a focus on charities that:

- incorrectly classified themselves as a Basic Religious Charity (and therefore did not report any financial information to the ACNC)

- operated in the 2017 reporting period but reported no financial activity

- reported the same financial information in 2016 and 2017.

Starting from the 2017 AIS, charities have been asked to report on their full-time equivalent (FTE) staff figure.

FTE staff refers to the number of full-time employees a charity would have if it combined the hours of full-time, part-time and casual employees.

For many charities, this figure appears on their PAYG forms. But it is also relatively simple to calculate manually. Charities can work out how many FTE staff they employ by adding up the total of all employee paid hours (including paid leave) for the relevant period, and then dividing this figure by the number of hours normally worked by a full-time employee.

We reviewed charities’ reporting of FTE figures to check accuracy and to identify if further guidance was required.

Results

We contacted 747 charities that had made errors in their 2017 AIS. In response, charities made corrections to their AISs involving:

- 51,484 FTE staff (many charities had included volunteer numbers when calculating their FTE)

- $20.7 billion in total revenue

- $670 million in total assets.

Of the charities we contacted:

- 69.5% were small

- 8.4% were medium

- 22.1% were large.

Improvements to the 2018 AIS

We improved the 2018 AIS in several areas, including:

- better validation to help charities detect and prevent errors before submission

- changes to the flow of the AIS to improve charities’ experience

- additional validation aimed at preventing charities from incorrectly reporting as a Basic Religious Charity

- extra guidance for FTE-related questions, with the AIS containing an inbuilt calculator to help charities work out their FTE staff numbers.

Selection Methodology

In previous years, our reviews have centred on the top 80% of charities registered with the ACNC. This year, the focus of our report is 2017 AIS and AFR submissions from medium and large charities.

In 2017, we focused on reviewing charities that had been subject to an AFR review in 2016. This aimed to ensure any errors identified in 2016 were rectified.

Our selected sample covers organisations from right across Australia. These organisations had a variety of legal forms, and a variety of reporting methods (including online and group reporting).

For the first time, 2017 saw us receive financial reports from non-government schools. This was a result of streamlined reporting initiatives developed in conjunction with the Non-Government Schools Working Group.

As part of the arrangement, the Commonwealth Department of Education and Training collected AFRs on behalf of the ACNC. We then reviewed a random selection of these AFRs to identify any extra guidance required to help non-government schools with their reporting.

What do we check for?

We checked both the accuracy of financial information reported by charities in the AIS, and the quality of AFRs, against these criteria:

- Accurate transposition of the financial information from AFRs to AISs

- Accurate selection of the type of financial report in the AIS

- Eligibility to use transitional reporting arrangements for financial reports submitted to a state or territory regulator

- Ensuring information provided in the AIS only relates to registered charities, especially where the consolidated financial statement prepared included non-registered entities.

- Provision of a complete set of financial statements as required by AASB 101 Presentation of financial statements

- Compliance with the mandatory reporting requirements for general and special purpose financial statements

- Provision of a signed auditor or reviewer report which includes references to the AFR meeting reporting requirements set out by the ACNC Act

- Provision of a signed Responsible Person’s declaration.

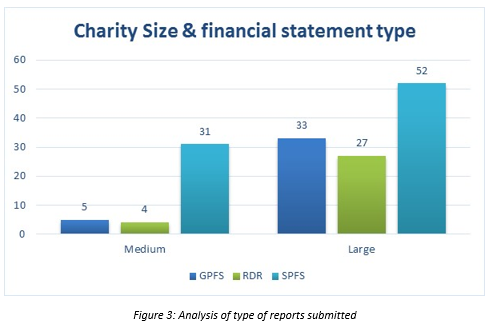

The ACNC reviewed 152 AFRs submitted by medium and large charities.

Figure 3 further details the types of financial reports reviewed for both medium and large charities.

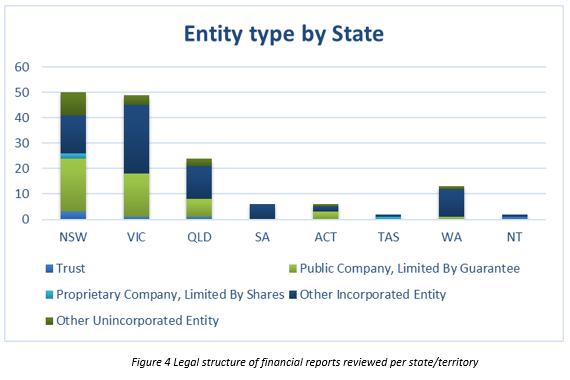

Figure 4 details the legal structures of financial reports included in the review, split into their locations.

Figure 5 (below) provides more information on the mean total revenue and assets of the financial reports reviewed.

| Mean Revenue | Mean Assets | |

|---|---|---|

| Medium | 638,277 | 1,688,255 |

| Large | 171,037,354 | 362,525,764 |

Note that the mean for large charities may be skewed, with three of the 152 charities reporting total revenue in excess of $2 billion. Total assets for two of those three charities were in excess of $5 billion.

Correct use of transitional arrangements

The ACNC has transitional reporting arrangements in place with several government agencies.

We also have streamlined reporting arrangements in place with South Australia, Tasmania and the ACT (since 2016), and with New South Wales and Victoria (since 2018).

Charities need to know the different types of transitional reporting arrangements as it affects the requirements of the financial reports they submit to the ACNC.

So that the ACNC could confirm that charities can take up transitional reporting arrangements, the 2017 AIS included questions asking:

- if charities reported to a state or territory regulator

- which state or territory the financial report was submitted to, and

- the reason it was submitted.

Of the 152 charities whose AFRs were included in our review, 69 (45.4%) said they reported to another regulator, 76 (50%) said they did not and seven charities (4.6%) did not respond.

But on review, 21.05% of charities were found to be eligible to use transitional reporting arrangements and 76.32% were not. This meant 70.39% charities responded to the question correctly, while 29.61% made an error.

Correct transposition of financial information from charities’ AFRs to AISs

Each year the AIS requires a summary income statement and balance sheet to cover a number of specific financial data elements. This also allows the ACNC to examine sector trends.

This year we compared financial information contained in charities’ AISs with their AFRs to check the accuracy of data transposition across:

- total revenue,

- total expenses, and

- total net assets/liabilities.

The results of the transposition checks for the 152 charities included in our review were:

| AIS matched to AFR | Total revenue | Total expenses | Net assets/liabilities |

|---|---|---|---|

| Correctly transposed | 81.58% | 82.89% | 84.87% |

| Incorrectly transposed | 14.47% | 13.16% | 9.21% |

| Not applicable | 3.95% | 3.95% | 5.92% |

Correct identification of charities’ financial statements as consolidated financial statements

Some registered charities are deemed to be ‘parent entities’ due to their control of other related organisations – for example, the way a charity’s head office might oversee branches or sub-branches of the same organisation, and can direct the operations of those organisations.

These parent entities prepare financial statements that group together the financial information of related organisations. These are known as consolidated financial statements.

Registered charities that prepare General Purpose Financial Statements (GPFS) are required to prepare and provide their consolidated financial statements to the ACNC.

Registered charities may also apply to the ACNC to report as a group and, once approved, provide us with the group financial report.

Through the AIS, the ACNC only collects financial information relating to registered charities. We included questions in the 2017 AIS to ensure that charities only provided us with information relating to registered charities.

Of the 152 financial reports reviewed, 27 were consolidated financial reports and 125 were single entity financial reports.

Just over 86.8% of charities correctly identified on their AIS whether consolidated financial statements were submitted, while 7.24% were not required to provide this information.

Of those that submitted consolidated financial statements, 73.9% correctly included financial information for registered charities. The remaining 26.1% may have incorrectly included information:

- of non-registered entities, or

- on entities other than the parent entity

Charities’ provision of complete sets of financial statements

AFRs must comply with AASB 101 Presentation of Financial Statements. This standard specifies that a complete set of financial statements comprises:

- a statement of profit and loss and other comprehensive income

- a statement of financial position

- a statement of changes in equity

- a statement of cash flows, and

- the notes to the financial statements.

Nearly 77 per cent (76.97%) of AFRs included in our review provided a complete set of financial statements.

And 96.05% of financial reports provided comparative information (noting that some charities may utilise transitional reporting requirements or the transitional relief for streamlined reporting).

The following table presents the percentage of charities that provided each financial statement.

| Financial Statement | Percentage |

|---|---|

| Statement of financial position | 99.34% |

| Statement of profit or loss and other comprehensive income | 97.37% |

| Statement of changes in equity | 83.55% |

| Cashflow statement | 84.21% |

| Notes to the statements | 96.71% |

Other observations

The type of financial report medium and large charities prepare can depend on whether the charity is a reporting entity.

If the charity is a reporting entity, it must submit GPFS that comply with all applicable Australian Accounting Standards. The accounting standards issued by the AASB include standards for the presentation, measurement and disclosure of financial statements.

When preparing GPFS, charities can choose to prepare either full GPFS or GPFS – RDR.

If a charity is not a reporting entity, it may prepare SPFS that meet the minimum reporting requirements set out in the ACNC Regulations.

The following table presents our observations of financial statements included in the review, and whether they met selected GPFS and SPFS requirements.

| Financial report checks | Yes | No | Unclear or Not Applicable |

|---|---|---|---|

| Classification of current and non-current assets and liabilities or liquidity presented in the statement of financial position | 98.68% | 1.32% | - |

| Line items presented in the Statement of profit or loss and other comprehensive income | 93.42% | 6.58% | - |

| Disclosures of significant accounting policies | 93.42% | 6.58% | - |

| Disclosure of appropriate accounting estimates and judgements management made in the process of applying the charity’s accounting policies | 75.66% | 22.37% | 1.97% |

| Cash flow statement classified between operating, investing and financing activities | 80.92% | 13.82% | 5.26% |

| Professional judgement applied in relation to potential impact of materiality on financial statements | 16.45% | 2.63% | 10.53% |

| Disclosure for the purposes of preparing the financial statements, whether it is a for-profit or not-for-profit entity | 58.94% | 41.06% | - |

| Disclosure of the statutory basis or other reporting framework, if any, under which the financial statements are prepared | 85.53% | 14.47% | - |

| Disclosure of fees to each auditor or reviewer of the financial statements (optional for GPFS – RDR) | 62.5% | 29.61% | 7.89% |

| Disclosure of compliance with Australian Accounting Standards when all Australian Accounting Standards have been complied with | 77.63% | 23.37% | - |

| GPFS only – Disclosure of key management personnel compensation | 89.71% | 10.29% | - |

| GPFS only – Disclosure of related party transactions | 37.5% | 1.97% | 60.53% |

| GPFS only – Disclosure of deprecation methods, useful lives or the depreciation rates used | 67.11% | 0.66% | 32.24% |

Auditor/reviewer report requirements

New auditing standards applied for financial reporting periods ending on or after 15 December 2016. The ACNC developed new templates which applied these revised standards.

Of the 152 financial reports examined in our review, 93.42% had an auditor or reviewer report attached. Of these, 99.3% were signed.

More than 63% (63.38%) of the audit reports complied with the new auditing standards.

Excluding charities utilising the transitional reporting arrangements, 55.92% of the auditor/reviewer reports referenced the ACNC Act.

Responsible Persons’ declaration

Nearly 93% (92.76%) of the financial reports reviewed featured an attached Responsible Persons’ declaration.

Of those that provided the Responsible Persons’ declaration, 95.04% were signed and 92.91% included a statement that the registered entity was able to pay all its debts, as and when they became due and payable.

For the charities that did not utilise transitional reporting arrangements, only 55.71% referenced the ACNC Act.

The ACNC has been working hard over the past year to improve the functionality and accessibility of the AIS and our website.

We have developed a checklist for the 2018 AFRs and AIS, which will help charities meet ACNC reporting requirements. The AFR checklist can be found as part of our AFR resources here: www.acnc.gov.au/financialstatements.

As the functionality of the online AIS continues to improve, we will focus more on providing information and guidance relating to the preparation and requirements of AFRs.