Each year, charities are required to submit an annual return to the ACNC – the Annual Information Statement (AIS). Medium and large charities are also required to submit an annual financial report (AFR).

The AIS contains a range of financial and non-financial information.

Data from each Annual Information Statement is used by the ACNC to ensure that charities are complying with the Australian Charities and Not-for-profits Act 2012 (Cth) (the ACNC Act), and to populate:

- the ACNC Charity Register

- www.data.gov.au

- the Charity Passport (allowing the ACNC to implement a ‘report once, use often’ framework).

The Charity Register is integral to maintaining and enhancing public trust in the charitable sector as it enables the public to view information on registered charities.

It also promotes transparency and accountability of the sector to donors and the public.

For the 2018 reporting period, 207 AISs and AFRs were selected for review and amendments made to the ACNC register to correct errors totalling $195,522,440 in total revenue and $614,226,373 in total assets.

This year, we made the following observations:

- 68% of charities selected the correct type of financial report to submit with their AIS. Of those that did not, the most common errors observed were the misclassification of General Purpose Financial Statements-Reduced Disclosure Requirement and Special Purpose Financial Statements as General Purpose Financial Statements.

- 21% incorrectly stated they were using transitional reporting arrangements, which is where the ACNC accepts financial reports prepared for and submitted to other regulators.

- These charities stated that they had to report to another regulator when in fact there was a streamlined reporting arrangement in place with that regulator – meaning their charity was only required to submit a financial report to the ACNC.

- 5% of charities incorrectly transposed information from the AFR to their AIS for the Total Revenue category, while 3% of charities made transposition errors for Total Revenue and Total Assets.

- 17% incorrectly identified their financial report as a consolidated financial report when it was in fact a single charity report.

- 42% of charities that submitted a consolidated financial report provided AIS income statement and balance sheet figures for the consolidated group as a whole rather than financial information on an individual charity basis.

- 75% of AFRs examined included a complete set of financial statements. Of the remaining 25%, the most common missing financial statements were those covering the statement of changes in equity and cash flow statement.

- Some common disclosure issues were:

- no disclosure on whether the charity was a for-profit or not-for-profit entity for financial reporting purposes.

- the legislative framework under which the financial report was prepared did not mention compliance with the ACNC Act.

- 94% of charities attached an auditor or reviewer’s report. More than 79% of those auditor’s reports complied with the new auditing standards, while 72% of the auditor’s reports provided an opinion on whether the financial report complied with the ACNC Act.

- 95% of charities attached a Responsible Persons’ declaration with 71% of charities mentioning compliance with the ACNC Act.

We will continue to review AFRs that charities submit to ensure compliance with the ACNC reporting requirements. We will also focus on ensuring that the financial information charities provide matches the information in their AFRs.

As at 31 January 2020, currently registered charities had submitted a total of 47,417 2018 AISs to the ACNC.

As shown in Figure 1 below, most charities are small, with lower levels of revenue and assets.

For medium and large registered charities required to submit an AFR, we received 15,152 financial reports. The table below shows the breakdown of the types of financial statements we received:

| Type of report | Number declared in AISs1 |

|---|---|

| General purpose financial statements (GPFS) | 6762 |

| General purpose financial statements – Reduced disclosure regime (GPFS – RDR) | 1358 |

| Special purpose financial statements (SPFS) | 7032 |

Our approach to reviewing the 2018 AIS and AFR

The ACNC has conducted reviews of the quality and accuracy of AIS and AFRs since 2015. In reporting the findings of these reviews, we aim to:

1 This assessment is based on the charities’ self-assessment of the type of financial report submitted from the 2018 Annual Information Statement

What did we check for?

In 2018 we reviewed 207 AISs and AFRs (an increase of 50 over the reviews which occurred in the 2017 financial year) to ensure:

- the AFR contained a complete set of financial statements:

- Statement of Profit or Loss and other comprehensive income

- Statement of Financial Position

- Cash flow Statement

- Statement of changes in equity

- Notes to the financial statements

- a signed audit or review report

- a signed responsible person's declaration.

- the charity had not made a material financial error when populating the financial information sections of the 2018 AIS (by comparing the AFR with the AIS)

- the charity had correctly reported the financial report type in the AIS (for example, general/special purpose)

- the charity had complied with the minimum accounting standards required under the Australian Charities and Not-for-profits Regulations 2013

- the charity was eligible for transitional reporting arrangements in reporting to state or territory regulators (refer to our website for more information),

- charities in South Australia, Tasmania or the ACT complied with the two-year transitional reporting to ACNC requirements)

- the charity had complied with related party disclosures required for general purpose financial statements

- the AIS did not include any financial information for non-registered entities (where a consolidated financial report was provided2).

Selection methodology

The types of charities we focused our 2018 reviews on included those that made errors in the 2017 AFR review. This approach ensures those errors have been rectified.

The ACNC has streamlined reporting arrangements for incorporated associations in the ACT, South Australia and Tasmania.

This allows charities in these states and territories to report solely to the ACNC, whereas previously they had to report to both the ACNC and their incorporated associations regulator.

Charities in these states and territories were provided with a two-year transitional reporting period to allow them to switch over to ACNC reporting requirements.

The two-year transitional reporting has now ended for charities in Tasmania. Charities in the ACT and South Australia are into their second year of the transitional reporting period (after which they will need to abide by the ACNC’s legislative requirements).

We have randomly selected AFRs from Tasmania, South Australia and the ACT to ensure that they meet the two-year transitional reporting requirement, or fully transition to the ACNC’s requirements.

2 The ACNC accepts consolidated financial statements from charities that are required to prepare financial statements in accordance with AASB 10, however the finance information in the AIS must only relate to the individual charity (the parent entity). For ACNC approved groups, the financial information in the Group AIS must only relate to registered charities.

The ACNC reviewed 207 AFRs submitted by medium and large charities. Thirteen of the AFRs submitted were from ACNC group reporters.

Figure 2 provides a breakdown of the types of financial statements selected for review for both medium and large charities.

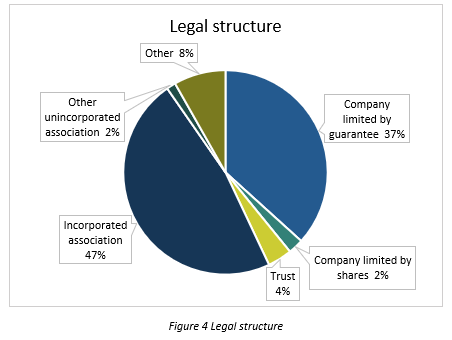

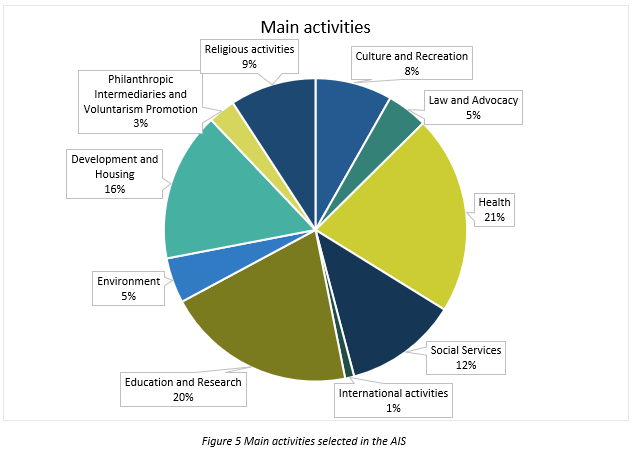

Figures 3-5 below provide the demographics of the financial report split by their locations, legal structure and their main activities.

The mean of total revenue and assets of the financial reports reviewed:

| Charity size | Mean revenue | Mean assets |

|---|---|---|

| Medium | $563,293 | $2,851,552 |

| Large | $55,729,206 | $98,008,036 |

Overall, 68% of charities selected the correct type of financial report to submit with their AIS.

The results below show a higher than average number of charities misclassified the financial statement type when submitting GPFS-RDR or SPFS.

In our previous dealings with charities that made this error, we found those submitting the AIS were not always familiar with the distinction between the different financial statement types.

The most common errors observed were the misclassification of GPFS-RDR and SPFS as GPFS.

Correct use of transitional arrangements

The ACNC has transitional reporting arrangements3 in place with several government agencies. This means we accept financial reports submitted to another regulator even though they may not meet the ACNC’s reporting requirements.

We also have streamlined reporting arrangements4 in place with Tasmania, South Australia and the ACT (since 2016), New South Wales and Victoria (since 2018) and the Northern Territory (from 2019).

Only charities using transitional reporting arrangements should state in their 2018 AIS that they are doing so. The 2018 AIS asks charities where and why they submitted their AFR.

Of all the charities (excluding group reporters) reviewed, only 18% were eligible to use transitional reporting arrangements.

Of those that were not eligible to do so, 21% incorrectly indicated they were utilising the transitional arrangements by stating that they had to report to another regulator because they were an incorporated association or a fundraising organisation even though they were no longer required to report to their state regulator (eg. SA, ACT, TAS incorporated associations)

This also applies to companies that selected they were a fundraising organisation. But companies are unable to utilise transitional reporting arrangements because they were previously required to prepare financial statements in accordance with the Corporations Act 2001. These statements are similar to the current ACNC reporting requirements.

Correct transposition of financial information from the charities’ AFRs to AISs

Each year the AIS requires a summary income statement and balance sheet to cover a number of specific financial data elements. This also allows the ACNC to monitor the sector’s financial health and examine sector trends.

This year we compared financial information contained in charities’ AISs with their AFRs to check the accuracy of data transposition across:

- total revenue;

- total expenses;

- total net assets/liabilities.

The results of the checks for all charities were:

| AIS matched to AFR | Total revenue | Total expense | Net asset/liabilities |

|---|---|---|---|

| Correctly transposed | 86% | 86% | 92% |

| Immaterial error | 11% | 9% | 5% |

| Incorrectly transposed | 3% | 5% | 3% |

In reviewing the financial reports of charities that incorrectly transposed income statement and balance sheet figures to the AIS, we found in some cases that the error occurred because the financial report may not have separately disclosed the same items required in the AIS amounts (as it is not required by the Australian accounting standards).

This meant some charities had to exercise their own judgement to aggregate or disaggregate the financial information within the financial report to allocate it back to the AIS. This process increased the chance of transposing errors in the AIS.

Correct identification of charities’ financial statements as consolidated financial statements

Charities (parent entities) that control one or more other entities (subsidiaries) may be required to present consolidated financial statements.

Charities that are reporting entities and/or GPFS are required to present consolidated financial statements to the ACNC.

Charities may also apply to the ACNC to report as a group and, once approved, provide a group financial report which could be on an aggregated basis rather than presenting on a consolidation basis.

Although we accept consolidated or combined financial statements which may include information relating to non-registered charities, the financial information provided in the AIS must only relate to registered charities.

Of all the financial reports reviewed, 20.3% were consolidated financial reports and 79.7% were single charity financial reports. More than 83% of charities correctly identified on their AIS whether consolidated financial statements were submitted. Just under 17% incorrectly identified their financial report as a consolidated financial report when it was, in fact, a single charity report.

AIS errors were identified for 42% of charities that submitted a consolidated financial report. In these cases, charities incorrectly provided AIS income statement and balance sheet figures for the consolidated group as a whole rather than financial information on an individual charity basis.

Charities’ provision of complete sets of financial statements

Annual financial reports must comply with AASB 101 Presentation of Financial Statements, unless the charity is eligible to participate in an ACNC transitional reporting arrangement or the first two years5 of a streamlined reporting arrangement.

This standard specifies that a complete set of financial statements comprises:

- a statement of profit or loss statement and other comprehensive income6,

- a statement of financial position,

- a statement of changes in equity,

- a statement of cash flows, and

- the notes to the financial statements

75% of AFRs examined included a complete set of financial statements. The following table shows the percentage of each financial statement included in the AFR.

| Financial statement | Percentage of submissions (full sample) | Streamlined reporting charities only* |

|---|---|---|

| Statement of financial position | 99.5% | 100% |

| Statement of profit or loss and other comprehensive income+ | 100% | 100% |

| Statement of changes in equity | 80.2% | 61% |

| Statement of cash flow | 83.6% | 67% |

| Notes to the statements | 95.2% | 93% |

* The results relate to charities that are incorporated associations in South Australia, Tasmania and the ACT, where the two-year transitional reporting period has ended, meaning charities should be complying fully with the ACNC reporting requirements.

+ Although all financial reports provided included a statement of profit or loss, a significant number of financial reports did not also include a statement of comprehensive income

Presentation of expenses

The accounting standards require charities to present expenses recognised in their profit or loss statement using a classification based on:

- their nature, or

- their function within the charity

A charity’s decision to present expenses by function or nature will depend on historical and industry factors, as well as the nature of the charity itself. Presenting expenses by both nature and function is not permitted.

Of the AFRs reviewed, 85% of charities reported expenses using the nature of expense method, while 5% reported expenses using the function of expense method. The remaining 10% of charities incorrectly reported their expenses.

Other observations

The type of financial report medium and large charities prepare will depend on whether the charity is a reporting entity.

If the charity is a reporting entity, it must submit GPFS that comply with all applicable Australian Accounting Standards. The accounting standards issued by the AASB include standards for recognition, measurement and disclosure requirements.

When preparing GPFS, charities can choose to prepare either full GFPS, or GPFS-RDR.

If a charity is not a reporting entity, it may prepare SPFS that must meet the minimum reporting requirements set out in the ACNC Regulations.

The table contained in the link below presents our observations of financial statements included in the review, and whether they met selected GPFS and SPFS requirements. (Click on the link to view or download the document)

Some items with high percentages of ‘No’ for GPFS are because:

- these results were drawn from our initial observations prior to contacting charities to correct their errors

- some charities stated in the basis of preparation that the financial statements prepared were GPFS. However, the statements were more likely to be otherwise upon closer review. That is because of a number of disclosures required for a GPFS were missing and some audit reports were stating they are not GPFS

- lastly, due to a small number of GPFS observed in this review, any errors captured will have an amplifying effect on the overall statistics. Therefore, these results should not be extrapolated to draw broader conclusions. Refer to Restriction of Use section for more details.

Auditor/reviewer report requirements

New auditing standards applied for financial reporting periods ending on or after 15 December 2016. The ACNC developed new templates which applied these revised standards.

Of the financial reports examined, 94% had an auditor or reviewer report attached. 99% of audit reports provided were signed, and more than 79% of the audit reports complied with the new auditing standards.

Excluding charities using transitional reporting arrangements, 72% of auditor/reviewer reports provided an opinion about whether their financial report complied with the ACNC Act.

Responsible Persons’ declaration

95% of financial reports examined included a Responsible Persons’ declaration.

98% of the Responsible Persons’ declarations provided were signed and 95% included a statement that the registered charity was able to pay all its debts as and when they became due and payable.

For the charities that did not utilise transitional reporting arrangements, 71% referenced the ACNC Act.

Results

We contacted 66 charities that had made errors in their 2018 AIS and/or AFR. In response, charities made corrections to their AISs involving:

- $195,522,440 in Total Revenue

- $614,226,373 in Total Assets

3 Medium and large charities may currently submit financial reports to their state and territory regulator, eg cooperatives. The ACNC may be able to submit the same financial report to the ACNC as meeting our requirements for the 2018 reporting period. This statistic excludes any non-government school charities utilising the transitional reporting arrangements.

4 The ACNC has entered into streamlined reporting arrangements where charities that are incorporated associations will only need to report annually to the ACNC via the AIS.

5 To date, the ACNC has provided a two-year transitional period for charities eligible for new streamlined reporting arrangements to help them transition to ACNC reporting requirements. See for example the NSW incorporated association transitional period guidance on the ACNC website.

6 Charities may present a single statement of profit or loss and other comprehensive income, with profit or loss and other comprehensive income presented in two sections.

The ACNC will continue to review charities’ annual financial reports to ensure compliance with the ACNC reporting requirements. We will also focus our efforts to ensure that the finance information provided by charities can be matched with the annual financial report.

We will continuously update the AFR checklist which will help charities meet our reporting obligations. This information can be found here: www.acnc.gov.au/financialstatements.

We have also developed a new Accounting and Auditing Standards webpage which provides information on new standards, as well as on changes to existing standards that affect charities as they prepare their AFRs.

Although some of the charity AFRs were selected at random, many were not. This is because some charities that had made material errors in their 2017 AFRs were selected for further review this year.

We therefore note the sample of AFRs reviewed as a non-probability sample.

It should be noted that non-probability sampling methods present challenges when attempting to draw broader conclusions about each group. We cannot say whether the results of our review accurately are reflective of the charity AFRs more broadly.

Caution should be exercised if attempting to use these survey results to draw general or broader conclusions.

The results from the analysis were taken at a point in time before any charities were contacted to correct any errors identified.

Charities may have stated in the basis of preparation that the financial statements prepared were GPFS. However upon closer inspection, the statements were more likely to be a SPFS because of a number of disclosures missing that are required for a GPFS.